Engineering the Exit: How to Get Acquired in Deep Tech

Cyril Ebersweiler, General Partner at SOSV, on the deep tech exit reality check, how founders build real buyer pull, and when to build more vs sell now.

Hey folks!

Thanks for being here.

For Issue #132 of Better Bioeconomy, I spoke with Cyril Ebersweiler, General Partner at SOSV, a global deep tech venture firm, and the founder and co-Managing Director of HAX, SOSV’s hard tech startup development program.

Cyril backs deep tech across hardware, robotics, biotech, and health, and has spent the past decade helping founders turn early prototypes into real companies. Last year, he launched RETVRN, a program designed to help early-stage deep tech and hardware startups prepare for exits.

I start with what RETVRN’s State of Exits 2025 data says about liquidity right now. Then, move into the exit mistake founders repeat, the traits that predict strong outcomes, when to build versus sell, what exit-readiness looks like, what buyers hammer in diligence, and which acquirer types are getting more active post-2022.

Let’s jump in!

Why exit planning matters

When the headlines are all unicorns and IPOs, it’s easy to treat acquisitions as the “backup plan.” But for most venture portfolios, M&A is the plan.

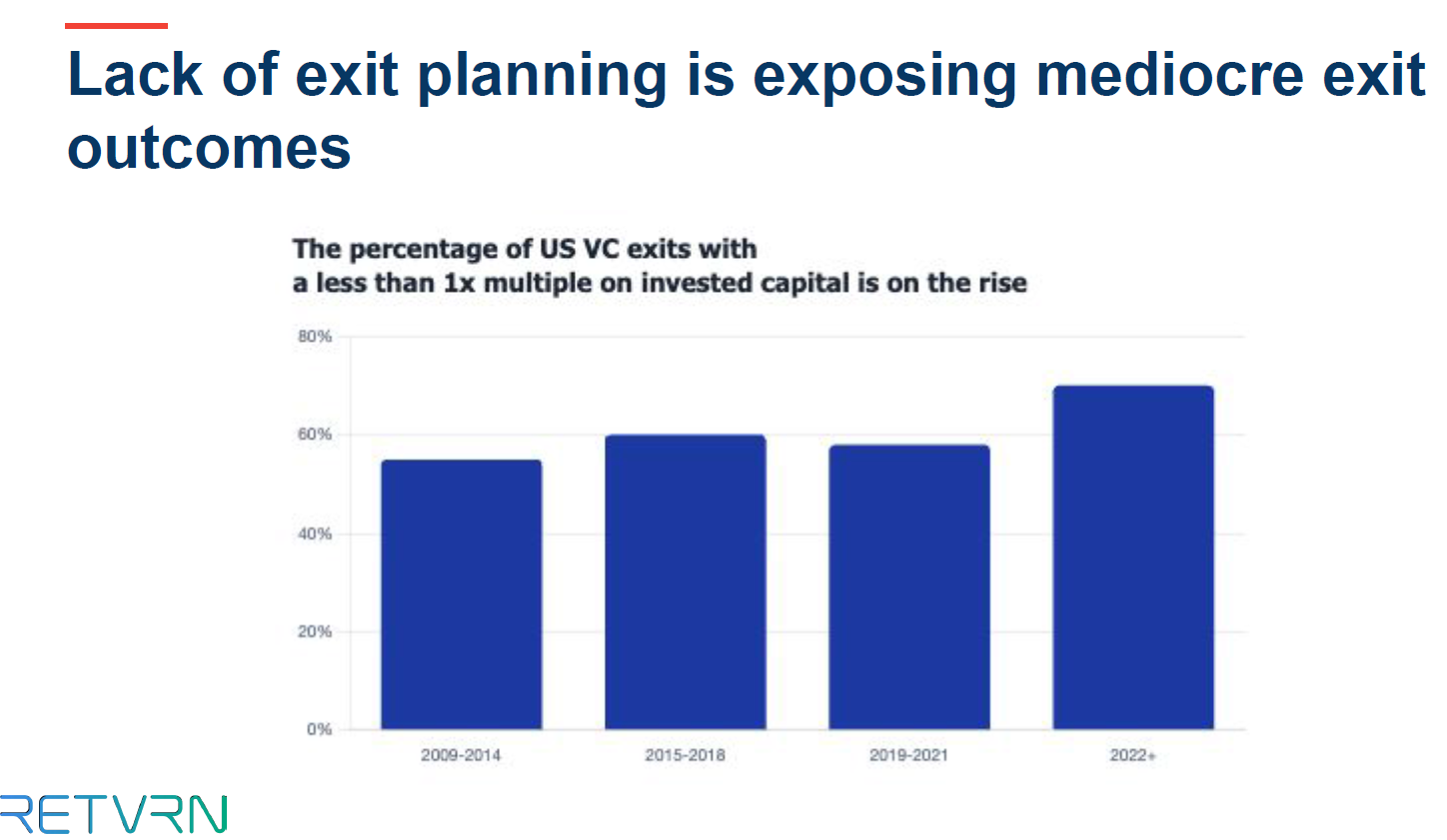

After 2022, that became harder to ignore. Valuations fell, risk appetite dropped, and buyers got pickier about what they’ll pay for. In that market, “we’ll think about an exit later” turns into “we’re scrambling when an offer shows up” or “we’re scrambling when the runway runs out.” Exit planning prevents both. It forces you to align early on what a great outcome looks like for your company, your team, and your cap table, before urgency limits your options.

An exit isn’t just a number on the paper. It’s the result of years of choices: ownership structure, IP paperwork, how clean the books are, how expectations are managed, and whether outsiders can understand what you’ve built. A sloppy process can leave founders with weak bargaining power, investors pulling in different directions, and a cap table that slows everything down.

A well-timed sale can do the opposite: put a technology inside a big distribution engine and get it into the world faster. As Cyril told me, “An exit to a strategic buyer is only the beginning of a new adventure, never forget that!”

Exits also keep the startup ecosystem alive. When founders and early teams get liquidity, some of that capital turns into new startups, angel checks, and operator talent recycled back into the next wave. When investors return capital to LPs, new funds get raised, risk budgets reset, and more startups get funded.

Before we jump into the conversation, here’s what RETVRN’s latest report says about the market.

What the exit market looks like right now

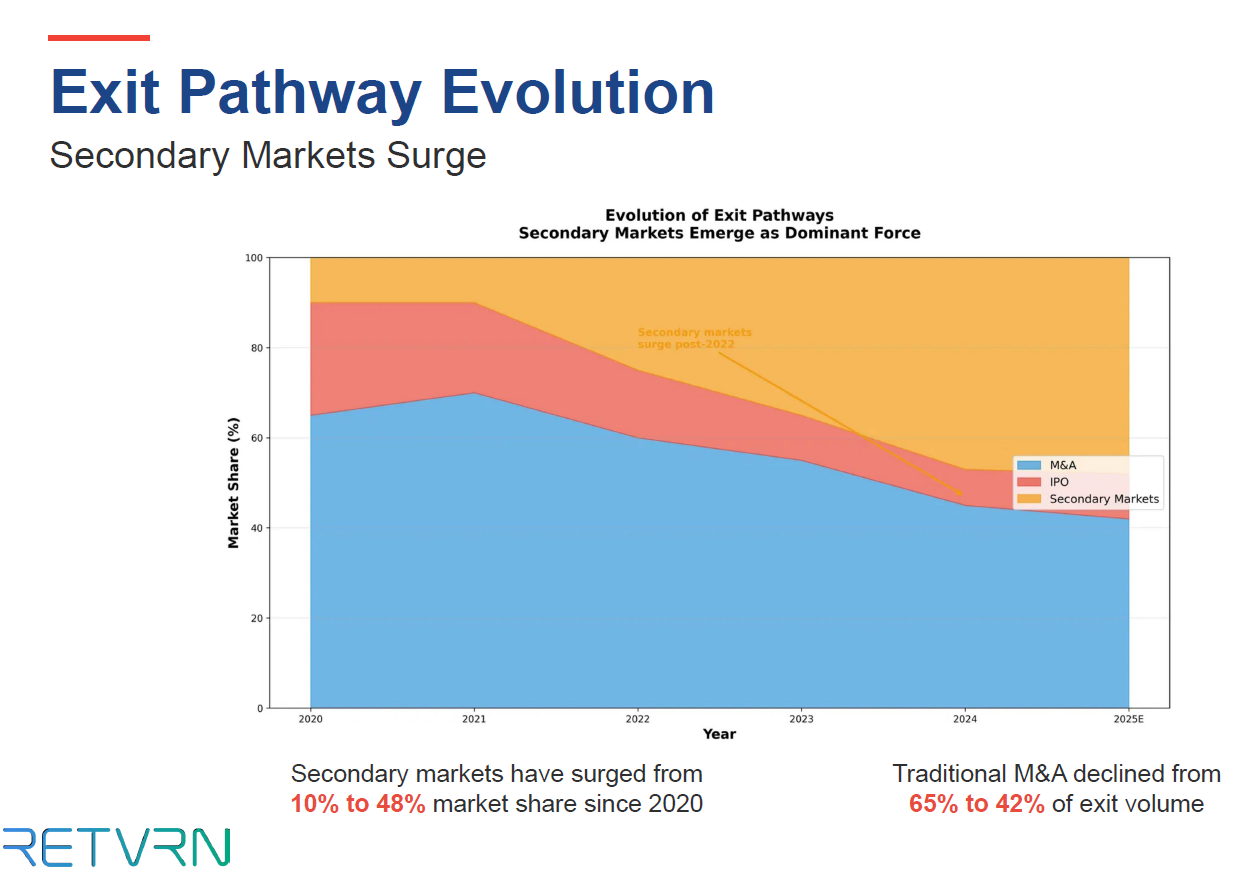

The report paints a stark picture of how value is captured. In 2024, 71% of exit dollars came from secondaries (investors selling shares to other investors), not IPOs or M&A, and 96% of M&A deals were under US$500M, and 70% were under US$100M.

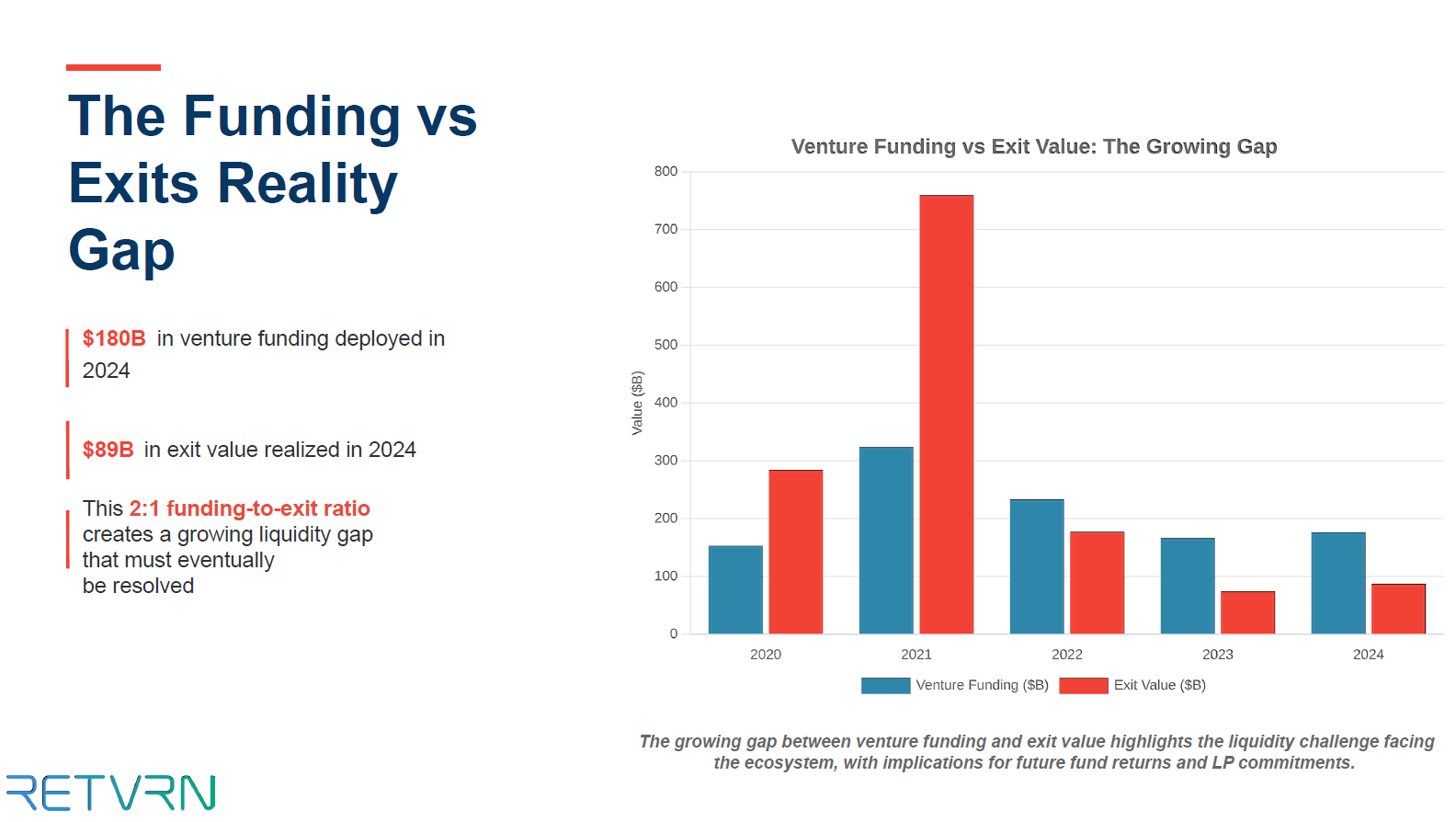

There’s also a massive liquidity gap between the capital flowing into startups and the value flowing out. RETVRN estimates roughly US$180B went into deep tech in 2024, while exit value was about US$89B, implying a funding‑to‑exit ratio of roughly two to one.

The shape of the exit market is changing, too. Global M&A volume fell about 9% in the first half of 2025, while average deal value rose 15%. This reflects a “flight to quality” in which buyers are doing fewer but larger deals.

Meanwhile, secondaries have also grown fast. The report puts them at 28% of exit volume (up from ~10% in 2020), and rising from 10% to 48% of overall exit market share.

Deal structures themselves are evolving. The report notes that 73% of transactions include earn‑out provisions (future payments tied to performance), and roughly 42 % of total consideration is contingent. Earn‑outs now average ~3.2 years and stretch across product milestones, revenue targets and integration milestones.

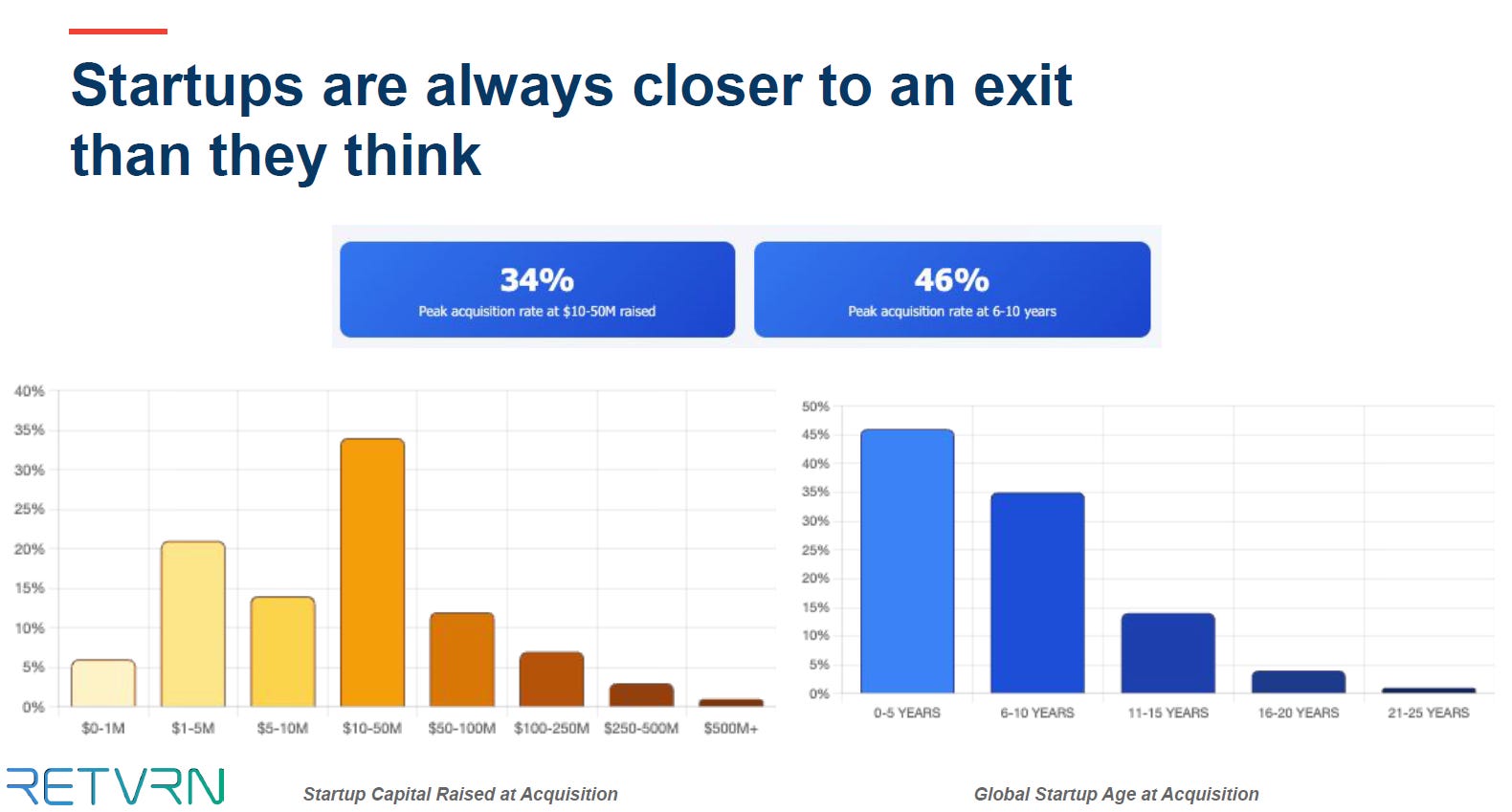

Timing is another surprise. More than 60% of acquisitions happen at or before Series A, and 47% involve seed-stage companies. The highest concentration sits below US$10-15M raised: 34% of deals happen there, and 46% of all deals happen within the first five years

Sector differences matter. RETVRN reports AI/ML companies reach median valuations ~3.2 times higher than the overall deep tech median. SaaS multiples fell from ~15 times revenue in 2021 to ~7 times. For biotech, the top quartile reaches 8-10 times the median. Time-to-exit differs too: AI often sells in 3-5 years, SaaS ~5.2 years, hardware 6-8, and biotech 11 years.

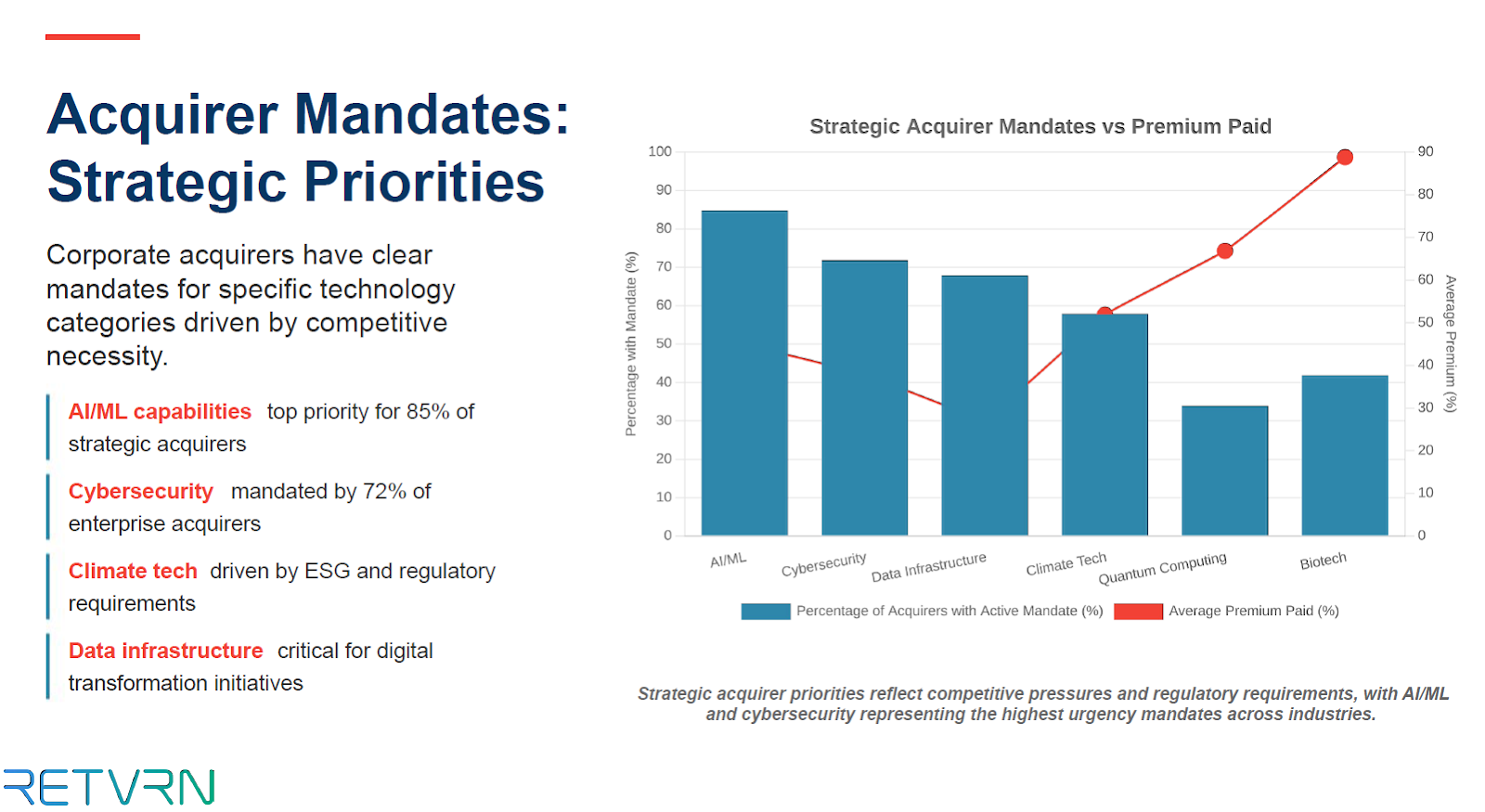

Finally, the buyer mix is also broadening. The report says 85% of strategic acquirers cite AI/ML as a top priority, and 72% cite cybersecurity. Sovereign wealth funds are showing up more often: direct investment into deep tech hit US$47B in 2024, and sovereign-led deals are up 3.2 times since 2020.

The most common exit mistakes

We kicked off our conversation with a simple question: What’s the single most common exit mistake you see? Cyril’s answer: “waiting too long to think about the exit.” Too many founders obsess over product and fundraising but neglect the downstream implications of how, when and to whom they might eventually sell.

“Founders often wake up at the last minute and realise they don’t know who their likely buyers are, or that their cap table is a mess. By then, it’s hard to clean up. You should start with an exit in mind and back‑track from there.”

In practice, that means sketching a buyer map early on. Who would benefit most from owning your IP? Which business unit wins if your tech exists inside their product line? What would integration look like? If you identify plausible acquirers in the first 12-18 months and track what they buy, you can make choices today that fit what they pay for later.

Another common mistake is failing to maintain a clean cap table. When investors, advisors and early employees accumulate layers of debt, warrants or SAFE notes with different terms, the eventual exit can get bogged down by renegotiations. A streamlined cap table with clear share classes, clear vesting, and no hidden obligations makes diligence smoother and increases the take‑home proceeds for everyone involved.

Finally, Cyril warned against neglecting governance. “Misaligned boards can kill an exit,” he said. If one investor won’t sell without a 10 times return, or co-founders no longer want the same future, even a fair offer becomes impossible to close. Talk through exit scenarios early, define decision rights, and agree on downside protections while everyone still has time to think.

What strong exits have in common

Cyril has seen dozens of exits across hardware and biotech through SOSV’s accelerators. So, what early decisions most consistently set up a company for a strong M&A outcome, even if it never reaches unicorn scale?

First, match the technology readiness level (TRL) to the capital you raise. Raising only what you need to reach proof-of-concept and early revenue (TRL 4-6) keeps expectations grounded. Huge rounds on speculative tech can price you out of what strategics are willing to pay.

Second, have a clear buyer logic. The most successful exits have a clear narrative connecting the startup’s capability to the acquirer’s strategy, which could be a technology bolt‑on, a market entry or a talent acquisition.

Third is early customer traction. Even in deep tech, a handful of paying customers changes the conversation. It shows the problem is real and gives buyers data they can underwrite.

Finally, relationships compound. People underestimate the time horizon of relationships. Introductions made in year one can pay off in year five. Joining pilot programs, co‑presenting at conferences and collaborating on open innovation initiatives are ways to get on the radar of potential buyers.

Navigating the trade‑off of building more or selling now

One of the hardest decisions founders face is whether to double down on building, i.e., raising more capital, expanding the product and aim for a bigger exit later, or to sell early.

Cyril suggested looking at three axes: technology maturity, market timing, and capital intensity. If you’re at TRL 4-5 and can reach TRL 7 with a reasonable amount of capital, staying independent may pay off because each milestone reduces buyer risk and can raise price. If the next step takes tens of millions and years of regulatory work, and buyers are already circling, selling could make more sense.

Another consideration is macroeconomic cycles. In the post-2022 market, deal volume fell, but strong companies still get paid for. If your investors are still anchored to 2021, waiting may not change much. If policy or supply-chain shifts are pushing on-shoring or local manufacturing, staying in the fight longer could capture more value.

Cyril suggested that founders ask themselves what their business will look like in three years if they do not sell, mapping out the capital required, milestones achieved and burn rate. Then map how the buyer set might change whether potential acquirers will be larger, hungrier or more regulated and whether new entrants such as sovereign funds or private equity will join the mix.

They must also assess whether they have enough runway and board alignment to make that journey, because if investors have limited reserves or different return horizons, pushing for an extra year may not be feasible.

Diligence red flags and how to avoid them

When a startup enters a sale process, the diligence phase can make or break a deal, and it’s rarely small. Cyril said even modest acquisitions can trigger 500+ diligence requests.

Common points of failure tend to show up in the same places. On the operations side, messy financials and a data room built at the last minute slow everything down. Buyers expect numbers accurate within ±10-15% and a process that can close fast.

On the legal and IP side, unclear IP assignment, contract loopholes, restrictive licensing, and filings that don’t match the story raise risk. Cap table surprises, such as odd clauses, side deals, and unclear proceeds flow, can derail terms. Strategy breaks when founders can’t explain why this buyer should buy now. And deals stall when leadership and governance aren’t aligned.

Treat diligence as ongoing work. Keep the data room current, track covenant compliance, and stay on top of IP filings.

Who buys deep tech now and why

With buyers more selective after 2022, Cyril sees two groups showing up more often: mandate‑driven strategics and sovereign and national‑security buyers.

Mandate‑driven strategics are big companies with clear goals in AI/ML, cybersecurity, data infrastructure, and “picks and shovels” categories that are buying to move faster. It’s not only Big Tech, but automotive and industrial companies are also buying robotics and AI to ship products and cut costs.

Sovereign and national‑security buyers include governments and sovereign wealth funds, which are playing a larger role in deep tech M&A. This group is often motivated by national self‑sufficiency or strategic advantage and comes with conditions like on‑shore manufacturing or technology transfer.

At the same time, private equity is increasingly active in deep tech, typically looking for profitable niche players where they can drive operational efficiencies and roll up adjacent capabilities. This group is particularly relevant for hardware companies that have reached breakeven but need scale to compete.

The net effect is a more fragmented but opportunity‑rich buyer landscape, and founders should broaden their horizon beyond the obvious names and consider corporate VCs, sovereign investors and PE funds.

What you can do today

Here is how you can operationalise your exit strategy starting today:

Build a buyer map early. In the first 12-18 months, list 5-10 strategic acquirers who would benefit most from your IP or market position. Don’t just list “Google” or “Bayer”, try to identify the specific business unit whose pain point your technology solves.

Build relationships ahead of need. Aim for active corporate development or strategic partnership threads 18-24 months before you want the option to sell. Pilots and JDAs are a practical way to prove value.

Keep your diligence basics clean. Treat your data room as a living document, not a project for the final hour. Ensure all IP assignments are signed, employee contracts are clean, and financials are accurate within a ±10-15% variance.

Check the capital treadmill before the next round. Map your TRL against the cash required to reach the next milestone. If the cost to reach TRL 7 forces major dilution that prices you out of 96% of the M&A market, weigh an earlier sale.

Make the bolt-on case easy. Your story should answer: where does this plug into the buyer’s product, and why does it pay off?

Get the board on the same page about the number. Talk about exit scenarios early. Ensure everyone is aligned on what a “win” looks like so you can act decisively when an offer arrives.

Want more investor perspectives like this? You might like my agrifood investor interview series, where I interview the investors backing the technologies reshaping food and ag. Recent conversations include PeakBridge, Big Idea Ventures, Ajinomoto Group Ventures, and more.

If you found value in this newsletter, consider sharing it with a friend who might benefit from it! Or, if someone forwarded this to you, consider subscribing.

Thank you very much Eshan for awesome issue #132. I must admit that a lot of Cyril's statements went over my head. But I'm grateful that people brighter than me are working hard to develop alt agriculture products and the funding required to build the infrastructure. I appreciate you Eshan for all the hard work you do to help educate us. Keep up the fantastic and extremely important job my friend. Have a very nice and peaceful week 😊 ❤️