Ag and Climate Tech Don't Have a Capital Problem, They Have a Capital Stack Problem

Renaissance Philanthropy's Joshua Elliott on treating the capital stack as one toolkit, when philanthropic capital fits startups, and why funders should think like an LP

Hey, it’s Eshan. Welcome to Issue #151 of Better Bioeconomy. Thanks for being here!

Last week, I sat down with Joshua Elliott, Chief Scientist at Renaissance Philanthropy and Director of its Advanced Research for Climate Emergencies (ARC) initiative.

This is the first time I have spoken to someone from the philanthropic side for the newsletter. Lately, I have been spending more time learning about the capital stack and the different funding models that support food, agriculture, and biomanufacturing.

As a VC, I think about where venture is the right fit for these sectors and where it is not. Venture is only one layer of a bigger stack. So I went into this conversation curious about the layers I understand least.

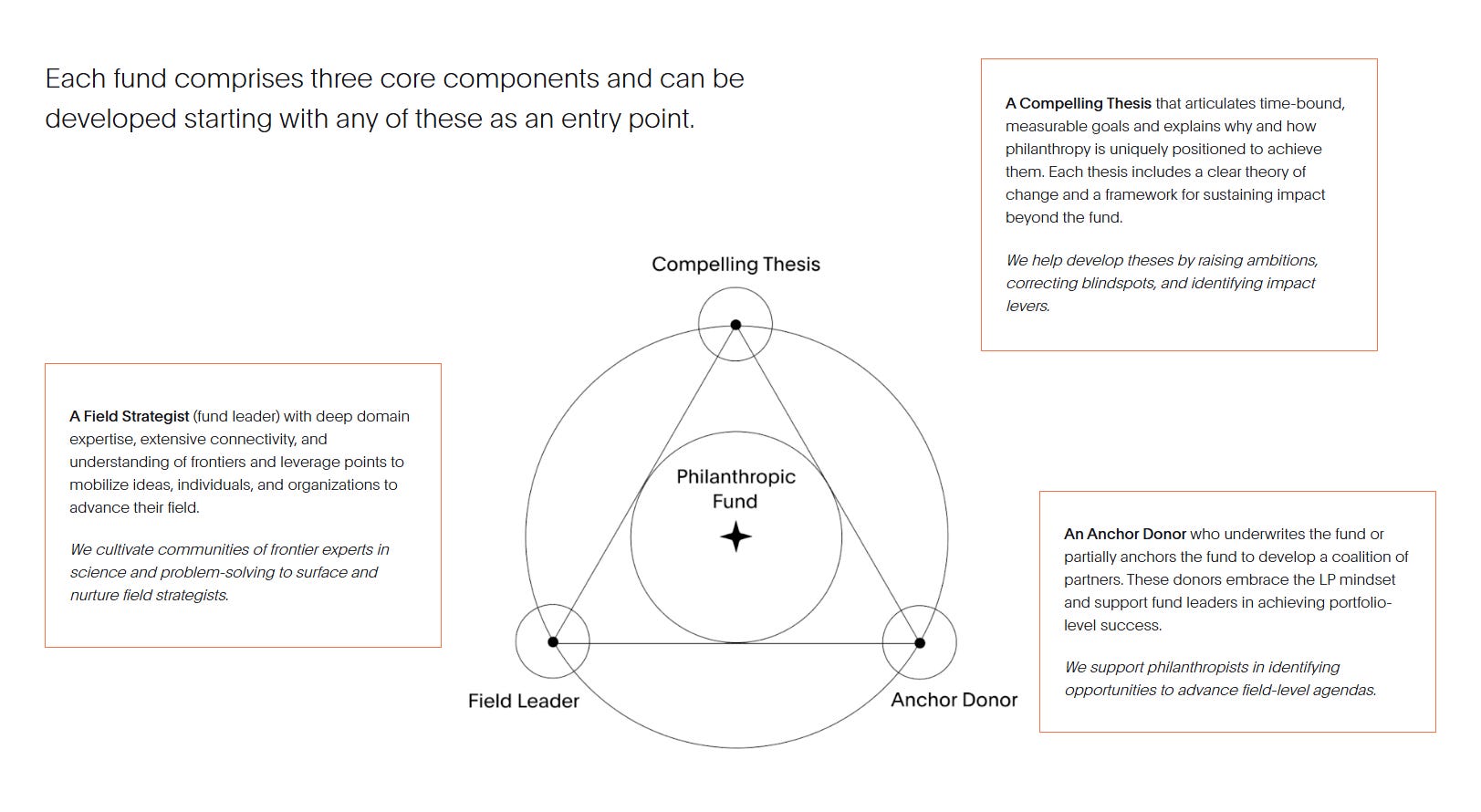

Renaissance Philanthropy is a nonprofit that designs, incubates, and runs time-bound, thesis-driven funds led by domain experts, with a stated goal of building the equivalent of venture capital for public good. The model is moving quickly. The organisation has mobilised $533m in the first two years, $268m of this directly for their own programs and funds, with $265m unlocked for other organisations. A meaningful part of that work is in agriculture and climate.

Joshua has watched the funding ecosystem from different angles. He took a PhD in theoretical particle physics, then spent a decade doing computational climate economics and crop modelling at the University of Chicago and Argonne National Lab, where he co-founded a centre for climate and energy policy and started the Global Gridded Crop Modeling Intercomparison Project.

Along the way, he ran his own ag-focused climate informatics startup, Praedictus Climate Solutions, as CEO. He then spent six years at DARPA as a programme manager, where he programmed close to $600 million in federal R&D, before a stint in climate philanthropy and his current role at Renaissance Philanthropy. He has been a startup founder, an academic grantee, a government funder, and now a philanthropic investor.

In our chat, we spoke about what that full-stack vantage point teaches him about how climate and ag tech get funded, when philanthropic capital is the right tool for a founder, how Renaissance Philanthropy turns philanthropic dollars into commercial companies, and what the capital stack could look like a decade from now.

Let’s jump in!

The sector has enough capital, but it just refuses to work together

Joshua’s organising idea is that climate and ag tech do not suffer from a shortage of money. They suffer from money that operates in silos. Venture, government, philanthropy, and project finance each optimise for their own logic, and nobody coordinates them around the path a single technology has to travel from lab to commercial scale.

A venture investor sprays and prays, a Series A fund only looks at Series A, and philanthropy, Joshua says, is sometimes the worst offender. “I’m a philanthropic investor, so all I think about is philanthropy. We silo all these forms of capital. They don’t work together.” The fix is to treat the whole stack as one coordinated toolkit instead of four silos optimised in isolation.

This goes wrong most often when the sector reaches for venture capital too early, for technologies that venture capital was never built to carry. Venture economics run on a low hit rate and a few massive winners, which is rational for a fund but brutal for a technology that just needs more time.

The casualties are not the bad technologies. “There’s a lot of potentially promising technologies that end up getting abandoned not because they don’t have promise,” he told me, “but because they couldn’t scale fast enough.” Joshua is the first to admit he does not have a tidy replacement model.

What he does propose is simpler: bring in patient capital earlier, and you give a good technology time to mature before the venture clock starts running against it.

Make the green thing the cheap thing, not the subsidised thing

Joshua calls himself a philanthro-capitalist, especially in climate, because for most climate tech, the road to real impact runs through scalable, profitable, market-rate products. He has watched the best version of this up close, working with family offices that run philanthropy, impact investing, and market-rate investing under one roof.

What he learned from them is the whole model in miniature: the same backers walk a single technology across all three pockets, using philanthropy to push it to the point where the impact investing team will fund it, then accelerating it until the market-rate team will. Each handoff is the proof. Philanthropy’s job is to hand the next investor down the line something they can back.

His worked example is cement, because it shows philanthropy doing something venture cannot. At the factory gate, he argues, the problem is (at least in part) already solved. There are cement products that are cost-competitive, 50% lower carbon, stronger, and longer-lasting than the traditional kind.

But they are not everywhere because of the pile of frictions sitting downstream of the factory: missing building standards, transport departments with no training to specify the new product, higher insurance, and higher capital costs.

Each adds an implicit cost that the technology itself does not. So Renaissance Philanthropy built a program that addresses all of those frictions at once. “We’ve created a systemic approach to look at all of those little downstream things that need to be solved, and then solving them all together and in tandem,” he said. That is field-building, the full-stack systems work Joshua and his co-authors lay out in their Philanthropy 2.0 essay, where one strategy spans science, policy, market-shaping, and adoption instead of stopping at the lab.

The goal underneath all of it is to make the clean option the cheap option, because that is the only version that lasts. Lean on a green premium and a subsidy, and the industry crumbles the day the policy changes.

He points to solar as proof that the durable path is cost, not subsidy. It became the world’s cheapest and fastest-growing source of energy, he points out, not because anyone was paying a green premium, but because four decades of work finally drove the price below fossil fuels.

The same logic should apply everywhere else. The way to win is to make the next cement plant, steel plant, or geothermal build cheaper as a low-carbon project than as a traditional one, so the economics make the choice for you.

The problem is time. “We cannot afford for all these new technologies to take the same four decades that solar took to move down that cost curve,” he said. That impatience is the whole reason for using philanthropic capital to push a technology down the cost curve faster, rather than waiting for the market to get there on its own.

For startups, philanthropic capital fits two specific moments

Philanthropic capital is rarely the first source of funding a founder thinks of, so when does it fit?

The first is at pre-commercial proof. If you have a real result but are three to five years from commercialisation, the Focused Research Organization is a strong option: a time-bound nonprofit startup funded in the tens of millions to prove one big thing, rather than the few million an academic lab scrapes from NSF (US National Science Foundation) grants.

He pushed back on the fear that founders have that taking philanthropic money means surrendering their moat. People assume open IP will ruin them, “whereas what they find later is that a large fraction of their moat is based on the tacit knowledge they’ve acquired along the way, not the specific admixtures or blueprints.” The know-how in the team’s heads is usually the more defensible part.

He also pointed founders to a growing set of government capital sources that, especially in the US, are far friendlier to commercialising IP than philanthropy is and are worth weighing alongside it.

He also flagged a related trap founders underrate: scaling is not just an engineering risk. “There’s actually a massive amount of new science risk that emerges in the process of trying to scale,” he said, “particularly in biology.” That is the risk patient, pre-commercial capital exists to absorb.

The second moment when philanthropic capital comes in is later, at the first demonstration plant, where the hurdle is the cost of money. Ask for capital to build the 200th traditional cement plant in a region, and lenders barely blink. Ask for capital to build the 3rd low-carbon plant, and you pay a premium, simply because the technology is less familiar.

Build in Africa or India, and the premium gets worse. “You can’t pay 16% interest rates on the capital you need for your demonstration plant,” he said, and most of the time, the math just collapses.

This is where a small amount of philanthropic capital can move a large number. By guaranteeing part of a loan, philanthropy absorbs some of the lender’s risk, which lets the lender drop the interest rate to something the project can carry. The capital is not spent, it is pledged as a backstop, and most of the time, it is never called.

The smart version of this taps money that is already sitting still. Joshua points to the roughly $250 to $300 billion parked in US donor-advised funds, charitable money earning 5 to 7% while it waits to be given away, a pool he expects to grow toward a trillion dollars as new AI wealth lands.

Renaissance Philanthropy runs a program, Tertiary Impact Capital, that leaves those funds untouched and simply uses them as the guarantee behind clean-tech loans. The donor’s money keeps earning its return, and the same dollars lower the cost of capital for a demonstration plant. “If you package things right,” he said, “you can get a pretty attractive set of investments and make a massive impact with a relatively modest amount of capital expenditure.”

When should a breakthrough become a for-profit company versus a public good?

Joshua is using philanthropic capital to spin out for-profit companies, which sounds like it should contradict the public-good rule. It does not, because the structure flexes to the situation. He has at least two live deals, each built differently on purpose.

The first is the partnership with Deep Science Ventures, the UK deeptech venture creator, with whom Renaissance Philanthropy built the Climate Emergencies Resilience Lab. In March, the two unveiled a venture creation project aimed at priming resilience in crops, a category meant to move past slow, static genetic modification toward resilience that can be tuned to climate risk.

Here, Renaissance Philanthropy takes equity at a fair market return. “Someday in the future, that equity will hopefully scale and be worth money, and then it can be returned to its philanthropic accounts, where it can be used to do even more philanthropic good,” he said. The company keeps its IP, because the philanthropy owns a fair share of the company.

The second, a pre-seed methane abatement startup, is structured as a concessional loan, and the asymmetry is the whole design. “If they succeed and scale, they will pay the capital back. If they don’t, then we made a philanthropic grant to something that didn’t produce a scalable for-profit company, so it’s fine.”

The downside is a grant, and the upside recycles into the next bet. The decision about whether something becomes a company follows the mission and the structure that gets the technology built.

The hard part is convincing people to deploy philanthropic capital

Two years in, the thing that has turned out to be harder than Joshua expected reframes the whole sector’s narrative away from a money shortage.

The hard part, he said, is convincing people to deploy philanthropic capital at all. “You look at the amount of capital that’s out there, and you think, oh, this can’t be that hard to do fundraising,” he said. “But it is, in fact, a lot harder than you think.”

Foundations pledge to spend $10 billion over a decade and are only three billion in seven years later. Philanthropy remains a network-driven, trust-based process, and for good reason: there is no single metric of quality the way there is in for-profit investing. That missing metric is, for Joshua, the root structural problem, and it is the argument he and Renaissance Philanthropy CEO Tom Kalil lay out.

For-profit investing specialised dramatically after the 1950s, from generalist banks into venture, then hundreds of fund types. But philanthropy did not do that. “We still use basically the model that Rockefeller developed in the 1930s,” he said, noting that the Gates Foundation and the NSF have each landed at roughly 2,000 staff giving away roughly $8 billion a year, the same basic architecture under different logos.

Kalil frames the gap as a shortage of institutions, not capital. Joshua’s own prescription follows from it: a GP/LP model, where philanthropists act as limited partners who build a portfolio of expert-led funds rather than vetting every grant themselves. “If philanthropists would think of themselves as more portfolio allocators rather than the ones selecting every single investment,” he said, “we would be much better able to scale philanthropic giving at the level that’s needed.”

Capital that follows the technology all the way to scale

If the Renaissance Philanthropy model works, what does the ag and climate capital stack look like in a decade? Joshua’s view is that philanthropic capital will be working across the whole stack rather than only to the left of the factory.

It will treat the cost of capital as a problem philanthropy is built to solve, especially the over-conservatism of capital in emerging markets and the Global South. It will write the small-ticket cheques that venture, even impact venture, cannot justify, the deals where the opportunity is real in places like Africa, but each one is too expensive to evaluate relative to its size.

Above all, it will fund the part everyone skips. Joshua’s frustration from his academic years was watching project after project build a clever solution, a new drought-tolerant seed or distributed fertiliser system, prove it in one town, declare victory, and walk away. “Without thinking about the incredible amount of work and capital it takes to scale that solution across tens or hundreds of thousands of towns across a region or a continent.”

That is where his critique lands closest to home. The valley of death in food and ag is not only a venture problem. It is a coordination problem across every pool of capital that could help cross it. Closing that gap is not about inventing the next drought-tolerant seed. It is about building capital that sticks around long enough to carry the good ones all the way to scale.

Want to connect with Joshua?

If this approach to philanthropic capital resonates with you, and you are a philanthropist or funder looking to deploy it, Joshua and the team would love to hear from you at info@renphil.org

If you found value in this newsletter, consider sharing it with a friend who might benefit from it!

Or, if someone forwarded this to you, consider subscribing.

Disclaimer: The views and opinions expressed in this newsletter are my own and do not reflect those of my employer, affiliates, or any organisations I am associated with.