The Great Unbundling: Ag Is Breaking Apart at the Top, While Consolidating Within Segments

Lessons from Verdant Partners’ 2025 Global Food & Agribusiness M&A Review & Outlook

Hey folks!

Welcome to Issue #137 of Better Bioeconomy, thanks for being here!

Today, I’m pulling apart one of my favourite annual reads, the Verdant Partners 2025 Global Food & Agribusiness M&A Review & Outlook. The report gives a practitioner’s view that most agrifood M&A commentary lacks. These are people who actually run sell-side and buy-side mandates across seeds, livestock, ingredients, equipment, and everything in between, across 30+ countries.

Reading this year’s edition, one theme kept surfacing across nearly every segment: the biggest M&A story of 2025 was separation. From Corteva splitting into two publicly traded pure-plays, to BASF preparing a Frankfurt IPO for its agricultural division, to Bunge and Viterra finally closing their mega-merger and immediately shedding overlapping assets (as part of antitrust requirements and integration), the industry is undergoing a structural unbundling that I think deserves a closer look.

But here’s what makes this more interesting: at the same time that conglomerates are breaking apart at the top, consolidation is accelerating at the segment level. Cooperatives are absorbing smaller retailers. Feed companies are rolling up regional players. Dairy cooperatives are merging into continent-spanning platforms. The unbundling is happening alongside consolidation, just at a different altitude.

Let’s dig in!

A practitioner’s read on a “suboptimal” year

Before getting into the analysis, a word on the source. Verdant Partners is a food and agribusiness-focused M&A advisory firm with offices across North America, South America, and Europe. They’ve completed over $4 billion in transactions across 30+ countries over 25+ years. (This is not a sponsored post!)

I look forward to their annual review because each section is written by someone with direct deal experience in a specific vertical. Dean Cavey on seeds, Blake Croegaert on grain handling and specialty ingredients, Graeme McCracken on agtech. Each section reads like a candid conversation with someone who just closed a transaction and has opinions about where the market is heading.

That practitioner lens is particularly useful for understanding the 2025 vintage of M&A, because the macro context was, to use Verdant Managing Partner Garrett Stoerger’s framing, “suboptimal.”

For many producers, 2025 felt like a replay of 2024. Commodity crop profitability suffered again from low prices driven by abundant supply and waning demand. High-value markets saw stable growth but felt the squeeze of persistently rising costs. Livestock producers experienced the biggest year-over-year improvement, but only after nearly a decade of pain. The overall industry mood had a carryover effect on everyone, from the farmers themselves to the upstream and downstream businesses that serve them, to the investors looking to deploy capital.

Verdant’s own framing centres on “portfolio rationalisation, capital discipline, and targeted growth.” The unbundling I’m focusing on is one manifestation of that broader rationalisation. But the targeted acquisitions happening simultaneously are the other side of the same coin, and they show up clearly in the data.

The biggest deals of 2025 were about subtraction, not addition

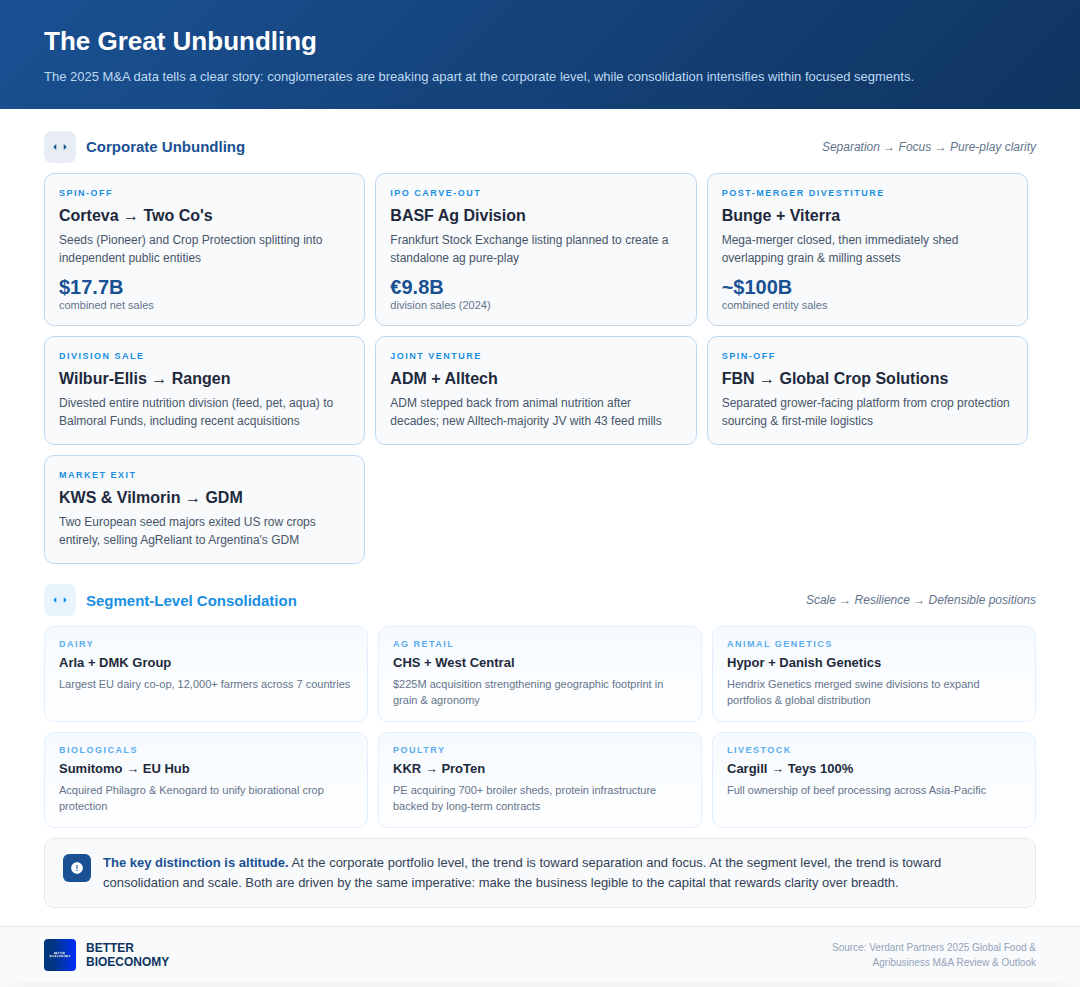

Let’s start with the moves that made the trade press. Corteva announced in October that its board had unanimously approved a plan to split the company into two independent, publicly traded entities.

“New Corteva” will retain the crop protection business, with estimated 2025 net sales of $7.8 billion. “SpinCo” will house the seed business, including the Pioneer brand, with projected 2025 net sales of $9.9 billion. The separation is expected to close in the second half of 2026.

Corteva itself was born from unbundling, spun out of DowDuPont in 2019, specifically to create a pure-play agriculture company. Six years later, the logic is being applied again, one level deeper. The seed and crop protection markets, Corteva’s leadership argues, have evolved to the point where the opportunities ahead for both businesses are diverging.

SpinCo is being positioned as a “classic growth compounder” that could expand beyond corn and soybeans into wheat, cotton, rice, fruits, and vegetables. New Corteva, meanwhile, will focus on operational excellence and biologicals. The underlying message is that these businesses need different capital allocation strategies, different risk profiles, and different investor bases.

Around the same time, BASF announced plans to list its Agricultural Solutions division on the Frankfurt Stock Exchange, with a target of being IPO-ready by 2027. BASF’s ag division generated €9.8 billion in sales in 2024. The company will remain the majority shareholder post-IPO, but the intent is to create a standalone, pure-play agricultural company with its own management board and strategic mandate.

Then there’s the Bunge-Viterra merger, which finally closed in July after years of negotiation and regulatory navigation. The combined entity will generate roughly $100 billion in sales. But the integration hasn’t been purely additive. As part of antitrust requirements and internal strategic review, Bunge divested five Canadian grain assets and its North American dry corn and masa milling business (acquired by GrainCraft).

Three different structures, a spin-off, an IPO, and a post-merger divestiture, all driven by the same underlying logic. The preference for focused, legible businesses is winning out over the conglomerate model at the corporate level.

The mid-market carve-outs that confirm the trend

The headline breakups get attention, but the pattern is just as visible in a series of less-publicised moves across the value chain.

Wilbur-Ellis divested its entire nutrition division to Balmoral Funds LLC, which rebranded the business as Rangen. The deal, which closed in August 2025, included animal feed, pet, and aquaculture ingredients businesses and assets. Wilbur-Ellis had acquired companies like F.L. Emmert (specialty pet ingredients) and Ametza (forage livestock pellets) within the prior two to three years, and both were included in the sale. Whether performance-driven or a strategic pivot back to its core retail business, the move brings more private equity capital into the specialty ingredients sector.

ADM and Alltech announced in September the creation of a new animal nutrition entity with 43 feed mills serving the US and Canada. The joint venture, majority-owned by Alltech, represents ADM stepping back from a segment it has operated in for decades. For ADM, this fits a broader pattern of portfolio simplification. For Alltech, it’s a chance to rapidly scale.

FBN (Farmers Business Network) announced the spin-off of its crop protection sourcing and first-mile logistics subsidiary, Global Crop Solutions. The spin-off creates two distinct companies, separating FBN’s grower-facing platform from its supply chain operations.

And in seeds, both KWS and Vilmorin & Cie (Limagrain) elected to exit the US seed corn and soybean market entirely, selling their jointly held AgReliant Genetics business to GDM, the Argentine plant genetics company. Verdant managed the transaction and describes it as perhaps one of the more surprising events in the seed sector in recent years. Two European seed majors decided that competing in US row crop genetics was no longer core to their strategy, opting instead to concentrate on their European corn businesses and other opportunities.

The common thread across all of these: shed what isn’t core, double down on what is, and make the remaining business attractive to capital that rewards clarity over breadth.

Conglomerates are breaking apart, but within segments, consolidation is increasing

Here’s where the picture gets more complicated. While conglomerates unbundle at the top, consolidation is intensifying within individual segments, and some of the year’s largest deals reflect this dynamic.

In dairy, Arla Foods and DMK Group announced a merger in April that will create the largest dairy cooperative in Europe, bringing together over 12,000 farmers across seven countries.

In crop inputs, Sumitomo Chemical fully acquired and consolidated its European subsidiaries Philagro (France) and Kenogard (Spain) to build a unified regional hub for its biorational and chemical crop protection business. Verdant’s Luboš Grepl describes this as one of the most significant M&A developments of 2025 in the biostimulants space.

In agriculture retail, CHS completed its $225 million acquisition of West Central Ag Services, further strengthening its geographic footprint and absorbing a smaller cooperative into a larger network.

These moves share similar logic. Arla and DMK are combining to achieve the scale needed to compete in a volatile dairy market. Sumitomo is integrating to build a coherent European platform. CHS is absorbing a smaller player to spread costs and strengthen resilience. At the segment level, scale still creates value, especially in asset-heavy, margin-tight businesses where financial strength determines survival.

At the corporate portfolio level, the trend is toward separation and focus. At the segment level, the trend is toward consolidation and scale.

What changed to make unbundling the dominant strategic response in 2025

So why is this happening now? I see three forces converging.

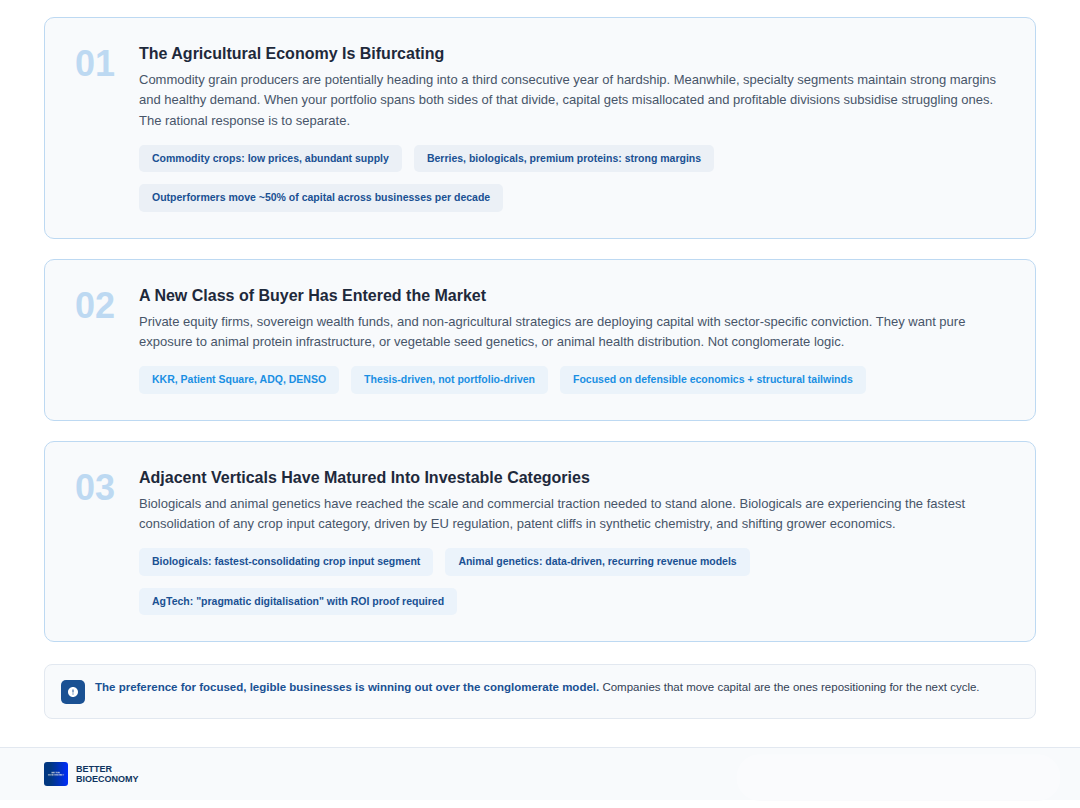

First, the agricultural economy is bifurcating in a way that punishes sprawl. Verdant’s segment-by-segment analysis paints a stark picture. Commodity grain producers are potentially heading into a third consecutive year of hardship. Meanwhile, specialty segments, including berries, high-value vegetable seeds, premium proteins, biologicals, and healthy snacking, maintain strong margins and healthy demand.

When your portfolio spans both sides of that divide, capital gets misallocated. Profitable divisions subsidise struggling ones. The rational response is to separate, letting each business compete for capital on its own merits.

This tracks with what I explored in Issue #131, where McKinsey’s analysis of 134 publicly traded agrifood companies showed that outperformers move roughly 50% of their capital across businesses over a decade. The Verdant deal log is essentially that thesis playing out in transaction form: the companies that move capital are the ones repositioning for the next cycle.

Second, a new class of buyer has entered the market, and they’re deploying capital with sector-specific conviction. Private equity firms like KKR and Patient Square, sovereign wealth funds like ADQ, and non-agricultural strategics like DENSO are all making investments in food and agriculture. These investors think in terms of focused theses, not conglomerate logic. They want pure exposure to animal protein infrastructure, or vegetable seed genetics, or animal health distribution. Stoerger’s observation that the current environment favours “well-capitalised buyers that have the market focus and operational expertise to extract incremental value” points to this dynamic.

Third, adjacent verticals, especially biologicals and animal genetics, have matured to the point where they can stand alone as investable categories. The biologicals segment is experiencing the fastest consolidation of any crop input category, driven by EU regulation, patent cliffs in synthetic chemistry, and shifting grower economics.

Agtech investment in 2025 was defined by what Verdant calls “pragmatic digitalisation,” with investors demanding proof of ROI and commercial traction, though it’s worth noting that Verdant’s Graeme McCracken is more cautious here. He observes that many AgTech categories still require additional scale, recurring revenue, and operating leverage before becoming attractive PE investment targets.

The buy side reveals where conviction capital sees durable value

Every unbundling creates a buy side. The buyers showing up for these assets tell us as much about the future of agrifood as the sellers do, and they fall into two distinct groups.

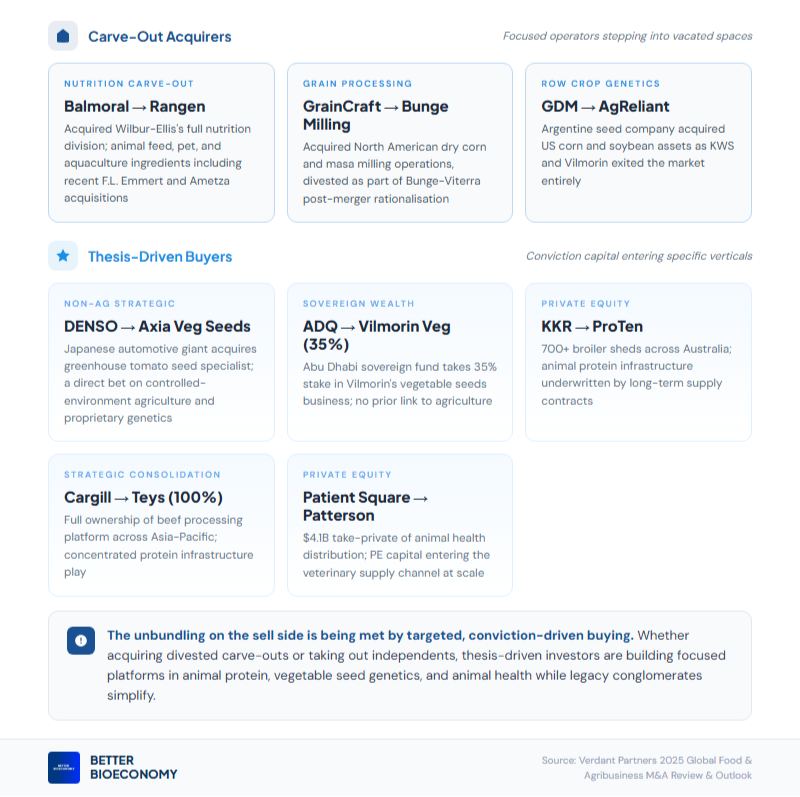

The first group is acquiring divested pieces from the conglomerate breakups. Balmoral Funds picked up Wilbur-Ellis’s nutrition division. GrainCraft acquired Bunge’s North American corn milling business. GDM bought AgReliant from KWS and Vilmorin. These are focused operators and financial sponsors stepping into the spaces that diversified companies have vacated.

The second group is taking out standalone businesses that fit a specific thesis, which is a related but distinct dynamic. DENSO Corporation, the Japanese automotive components giant, entered the vegetable seed industry with its acquisition of Axia Vegetable Seeds, a specialist in high-quality tomato seeds for greenhouses. This kind of entry by non-traditional players signals growing interest from outside the industry in acquiring differentiated breeding platforms and advanced R&D pipelines.

Abu Dhabi’s sovereign wealth fund ADQ entered exclusive discussions with Vilmorin & Cie for a 35% stake in its vegetable seeds business. Vilmorin delisted in 2023 and is now significantly connected to a sovereign fund with no previous link to agriculture.

In Australia, KKR acquired ProTen, one of the country’s largest poultry and agricultural infrastructure businesses, with over 700 broiler sheds. A financial buyer underwriting the long-term structural demand for animal protein through infrastructure assets backed by long-term contracts. In the same region, Cargill acquired full ownership of Teys Investments, consolidating its beef processing position across Asia-Pacific.

And Patient Square Capital completed a ~$4.1 billion take-private of Patterson Companies, a leading North American and UK supplier of dental and animal health products. The animal health distribution channel is attracting PE capital at scale.

Both dynamics point in the same direction. Whether they’re acquiring divested carve-outs or taking out independent companies, thesis-driven buyers are building focused platforms while legacy conglomerates simplify. The unbundling on the sell side is being met by targeted, conviction-driven buying on the other.

What I’m watching in 2026

Conglomerates are breaking apart, but within focused verticals, integration is still the winning logic

The most visible trend in Verdant’s data is ‘deconglomeration’: diversified players shedding unrelated divisions and retreating to core competencies. But the flip side of that story is equally important. Within those focused verticals, the appetite for capability-building acquisitions has not diminished. What’s changing is the unit of integration, from portfolio breadth to segment depth.

For founders, this distinction matters because the acquirers most active in 2025 were filling specific gaps in existing platforms. Understanding exactly where those gaps sit in your most likely acquirer’s stack is increasingly the work.

Biologicals M&A is approaching the moment that separates conviction from momentum

Biologicals attracted some of the most significant deal activity in 2025, and the strategic rationale from major acquirers sounded coherent. But now will be the real test of whether those acquisitions perform commercially at scale. The products need to prove consistent field results, the supply chains need to hold, and the bundled go-to-market strategies need to generate the revenue lifts that justified the acquisition multiples.

If that proof arrives, the category enters a self-reinforcing cycle where channel confidence rises, and farmer adoption broadens. If it doesn’t, expect a quieter deal environment as acquirers absorb write-downs and the next wave of biologicals startups finds fundraising harder.

The 2025 buyer universe is a spec sheet for what to build toward

Looking across the deals Verdant tracked, the acquirers with the most conviction and the clearest strategic rationale were paying for a fairly consistent set of attributes: proprietary data assets, defensible biological IP, demonstrated commercial traction in a specific crop or geography, and technology that slotted into existing workflows rather than requiring a full practice change.

For founders thinking about exit readiness over a five-to-seven year horizon, that list is more useful than any generic “build a moat” advice. The buyers who showed up in 2025 told what they were missing. The question is whether you’re building toward that gap.

If you found value in this newsletter, consider sharing it with a friend who might benefit from it! Or, if someone forwarded this to you, consider subscribing.