Agritech Didn't Fail in Southeast and South Asia. The Capital Did.

Lessons from ‘The Opportunity for AgriTech Investment in Southeast and South Asia’ report by Beanstalk AgTech and Briter Bridges.

Hey folks!

Welcome to Issue #142 of Better Bioeconomy, thanks for being here!

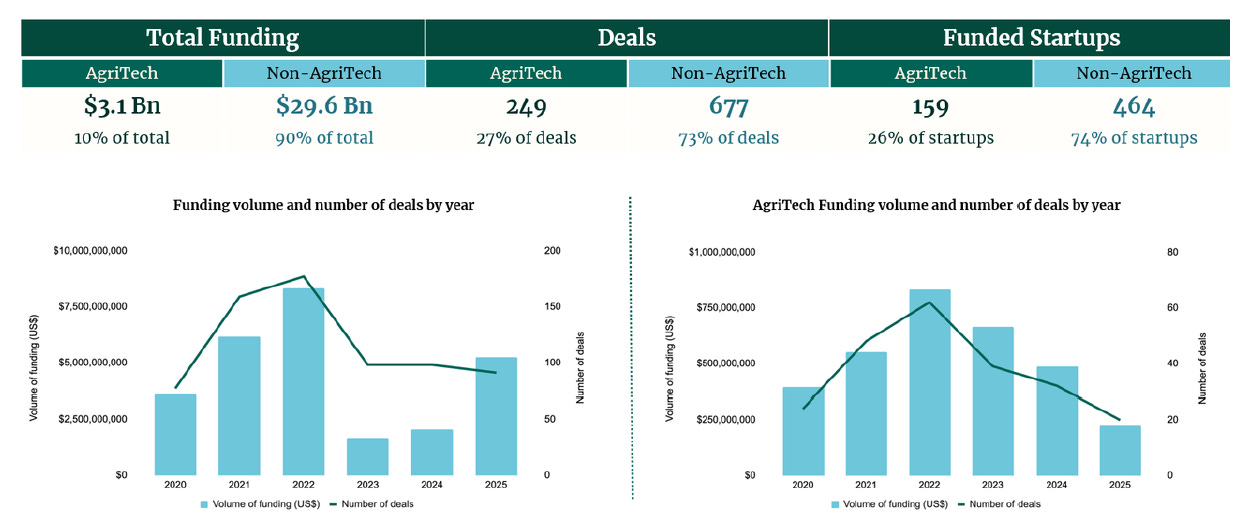

Agritech funding in Southeast and South Asia (SEASA) peaked at more than $750 million in 2022, then dropped roughly 70% by 2025 in both deal count and funding volume. Most people read that as a market failing.

But reading the recent report, “The Opportunity for AgriTech Investment in Southeast and South Asia” (published by Beanstalk AgTech and Briter Bridges, commissioned by Omnivore, FMO, IFC, and Rabo Foundation), I kept arriving at a different conclusion. The opportunity metrics haven't moved. What pulled back was a specific capital model that was not built for how value gets created in these markets.

That difference between a market correcting itself and a capital model revealing its own structural limits is what I want to explore. Because what SEASA is teaching us about capital architecture in emerging agricultural markets is relevant beyond the region.

Let’s dig in!

The funding dropped 70%, but the opportunity metrics didn’t move

The report covers the SEASA region: Southeast Asia (Vietnam, Indonesia, Thailand, Philippines, Myanmar, Cambodia) and South Asia (India, Pakistan, Bangladesh, Sri Lanka), drawing on deal-level data, crop-specific value chain analysis, and a mapping of the startup and investor ecosystem.

Agriculture contributes ~15% of GDP and employs 30-42% of the workforce across SEASA. Between 2020-2022, generalist VCs poured capital into the region. When funding collapsed by 2025, the pullback was sharp and broad. But the structural drivers of the opportunity stayed put.

Yield gaps, post-harvest losses, and SME financing shortfalls remain largely unchanged. The report estimates that digitalisation and agritech adoption could unlock more than $90 billion in annual GDP gains in Southeast Asia alone by 2033.

The report makes another observation I can attest to: agritech rarely ranks as a priority sector for venture capital allocation. It sits at the bottom of what the authors call the “investment waterfall,” with capital flowing first to climate tech, fintech, and broader impact sectors. In my experience, even within climate tech across the region, most allocator attention goes to energy and transportation, with agrifood treated as an afterthought despite its outsized impact potential.

So the capital that flooded in during 2020-2022 was not just the wrong structure. For many funds, agritech was never the core conviction. The 70% funding drop was a failure of the capital model on its own terms, not a market failure.

SEASA is a collection of distinct, localised markets, each with its own rules

The report clearly maps the fragmentation of the region. SEASA is not a market. It is a collection of distinct, localised markets, each with its own policy regimes, value chain dynamics, and consumer patterns.

The report draws a foundational distinction between two types of agricultural markets that coexist across the region. Smallholder-led staple value chains, rice, maize, and wheat in Bangladesh, Cambodia, and Nepal, are high volume, low margin, and oriented toward domestic food security. Highly commercialised, tech-adopting chains, rubber, coffee, and palm oil in Thailand, Vietnam, and Indonesia, are export-oriented, compliance-driven, and increasingly venture-legible. Same region, different investment theses.

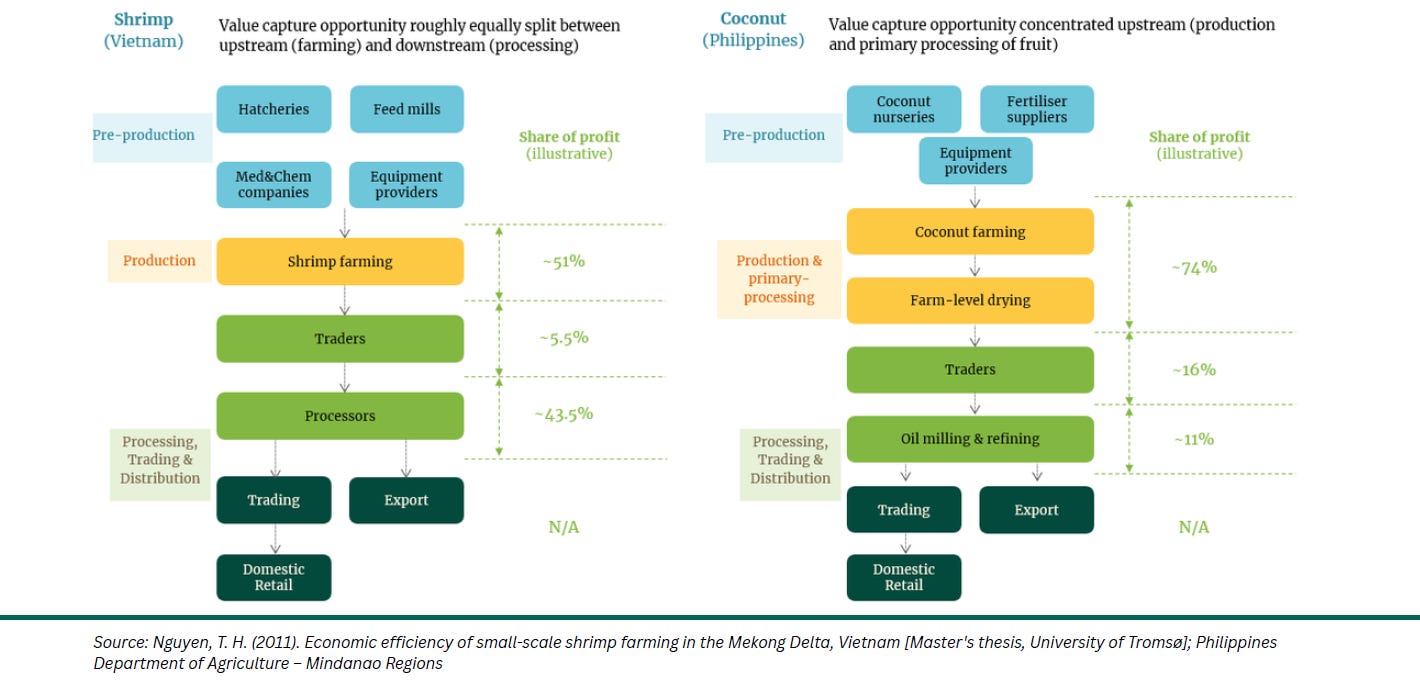

The fragmentation runs deeper than that divide. Even within a single crop, where value concentrates in the supply chain varies by country. In Vietnamese shrimp farming, profits split roughly evenly between upstream production (51%) and downstream processing (43.5%).

In Philippine coconut production, 74% of the profit pool sits upstream in production and primary processing. The point is not to compare shrimp with coconut. It is that the investment thesis has to be crop-specific and country-specific. Backing a downstream aggregation play without understanding where the profit sits in that specific value chain could lead to misallocation of capital.

Premature regional expansion was one of the most common failure modes. Of the entire SEASA ecosystem, only 12 startups attempted cross-border scaling, with approximately two-thirds failing or pulling back. This matches what I’ve seen working in the region. The pitch deck says “Southeast Asia,” but moving from Indonesia to Thailand could mean rebuilding distribution, regulatory relationships, and tweaking the product itself.

In SEASA, the funding that arrived in the first wave was structured for regional scale. The assumption was that a model proven in Vietnam could be replciated into Indonesia, then the Philippines. The markets disagreed.

Strong local traction, failed regional expansion

That fragmentation created the conditions for a specific and repeatable failure pattern. The vast majority of SEASA startups surveyed operate at negative margins. By 2022-2023, 69% of the $569 million in funding went to startups with demonstrated unit profitability, suggesting investors had already learned to screen for it.

The report identifies what it calls the "Series C Trap." Early-stage companies achieve strong local growth by solving a specific friction point in a single market. Earlier rounds up to Series A can generate real traction. The trap springs later: under pressure to demonstrate the scale that justifies a Series C valuation, companies attempt cross-border expansion into markets with fundamentally different dynamics. Distribution costs can consume 30-40% of revenue in fragmented SEASA markets, and the result of premature expansion is diluted product-market fit and eventual failure.

What the first wave exposed: unit economics matter more than the total addressable market. The region has 71 million farmers, but only ~5% use digital platforms with an average spend of below $50 per year. The addressable market was a fraction of what pitch decks suggested. Direct-to-farmer models made it worse: customer acquisition costs ran 3-5x higher than B2B or intermediary approaches, and even after acquisition, serving smallholders at that price point was economically challenging. Onboarding, support, and logistics costs eroded whatever margin remained.

Over 60% of failures between 2022-2025 cited poorly sequenced scaling as the cause. The companies that survived share a pattern: they dominated a single market before expanding, built local execution teams, and treated distribution as a core competence rather than a fundraising milestone.

The typical Series C timeline assumes that the infrastructure for scaling already exists: reliable distribution, functioning logistics, and available financing for customers. In SEASA, that infrastructure often does not exist. The VC scaling cadence collided with markets that require ecosystem-building before, or at least alongside, company-building. There's a related dynamic I see often: VC pressure makes startups feel they need to ramp faster than their demand requires, leading to CAPEX investments in capacity that sits underutilised. The capital model doesn't just fail at the wrong stage. It can distort operating decisions well before that stage arrives.

Three demand drivers that exist regardless of VC sentiment

Despite everything the first wave got wrong, the structural drivers of the opportunity were never the problem. Reading across the report's value chain analysis, three pillars stand out, each grounded in constraints that technology can address, and each growing independently of venture capital sentiment.

What connects all three is that they are pull markets: the demand exists independently of whether a startup shows up to serve it.

Productivity gaps and the $40 billion in annual losses

Production yields across SEASA remain 2-6x lower than the highest-yielding global producers, and post-harvest losses add $40 billion in annual drag from inadequate cold storage and fragmented logistics. But not all of that gap is the same kind of problem.

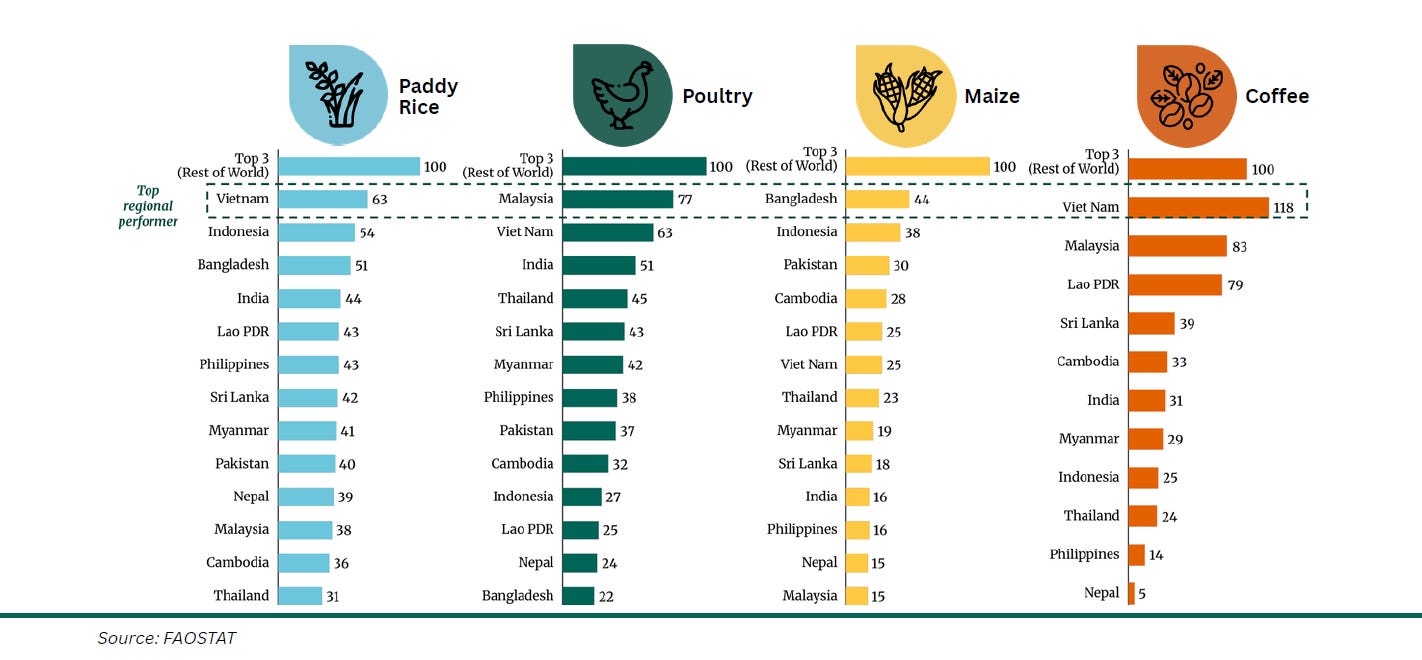

Countries with high Total Factor Productivity (TFP) growth, like Vietnam, are modernising: output is rising while the labour index is declining, signalling a sector where labour is becoming more productive. The technology opportunity here is precision agriculture, input efficiency, and automation.

Countries with low TFP growth, like Pakistan, are growing through extensification: output gains are matched by increases in labour and land inputs. The opportunity there is more foundational: basic mechanisation, improved inputs, and knowledge dissemination platforms.

This matters for investors because it means the same sector label (”productivity tech”) describes two completely different investment theses depending on the country.

Premiumization and compliance as a paid market

Beyond yield gains, value is increasingly created through premiumization, particularly for high-value export crops like coffee and palm oil. The rise of mandatory compliance pressures, most notably the EU Deforestation Regulation (EUDR), has turned what was once an optional ESG upgrade into a non-discretionary requirement.

Technology solutions for MRV (Measurement, Reporting, and Verification, the tools that track, measure, and prove environmental claims) and traceability are creating what is effectively a paid market for compliance. B2B SaaS platforms that bundle compliance software with verification services can capture value through mandatory traceability adoption. The scale of the premium can be seen in specialty categories already: coconut sugar commands 1,600-5,000% premiums, and premium seafood 650-20,000% over commodity equivalents.

When a regulation requires compliance, the willingness-to-pay question largely disappears. But the open question is who captures that value. If the tech provider is enabling a premium that accrues to the exporter, the SaaS fee has to be priced against margin the exporter would not otherwise have. That is a strong position, but only if switching costs are high enough to prevent the exporter from building the capability in-house once the compliance workflow is proven.

Climate adaptation is creating “market pull” for non-discretionary tech spending

Drought, salinity, cyclones, and extreme heat impose unavoidable adaptation costs across SEASA agriculture. The report frames this as a “pull” market: climate technologies are shifting from optional to essential expenditure.

What makes this useful for investors is that the climate patterns themselves dictate distinct technology priorities by geography. Drought-resistant genetics and water optimisation (like Alternate Wetting and Drying for rice) map to mainland Southeast Asia and inland South Asia, where water stress is most acute. Salt-tolerant crop varieties target coastal regions facing dual threats of flooding and salinity from sea-level rise. Storm-resilient infrastructure and parametric insurance concentrate along exposed coastlines in the Philippines, Vietnam, and eastern India, where cyclone vulnerability is highest.

Each of these is a different product category, a different customer, and a different go-to-market. The climate thesis in SEASA is not one investment. It is at least four, each geographically constrained.

That said, policy design matters as much as climate exposure. Vietnam’s One Million Hectare rice program has successfully catalysed smart cultivation and traceability pilots at national scale. Pakistan’s biofertilizer startups face headwinds from entrenched chemical subsidy regimes. Same regional challenge, opposite policy environments, very different adoption curves.

The harder question remains adoption velocity: parametric insurance has been “gaining traction” for years, but actual penetration among smallholders remains thin. How fast structural demand converts into revenue depends on distribution infrastructure that, in much of SEASA, does not yet exist. This is the same constraint that doomed direct-to-farmer platforms in the first wave. The opportunity is real. The business model that can access it without building infrastructure from scratch is what separates a viable business from an expensive lesson.

Three verticals where the economics work

Not all SEASA agritech verticals are waiting for the same kind of capital to come back. What connects the verticals showing signs of life is strong underlying economics. What separates them is the capital structure each one requires.

Aquaculture and marine innovation

Aquaculture contributes $26.9 billion annually to Indonesia’s economy alone and employs millions across Vietnam, India, and Bangladesh. This is the vertical where the gap between potential and current utilisation is widest. Indonesia’s seaweed industry alone could reach $11.8 billion by 2030, yet only 0.8% of suitable hectares are currently utilised.

Feed accounts for up to 57% of total costs for shrimp and 84% for pangasius (a freshwater catfish native to Southeast Asia), so any efficiency gain in feed conversion translates directly to margin. Platforms like Tepbac (Vietnam) and AquaEasy (Singapore) claim feed savings of 20-30% through AI-driven farm management.

The sector is also adapting its business model in response to first-wave lessons. 61% of aquaculture startups now offer bundled solutions combining hardware, software, inputs, and services, with marketplace-plus-SaaS platforms attracting the largest rounds.

Despite high-profile failures in the sector, the demand for aquaculture protein continues to grow, and the production inefficiencies remain massive. But the capital this vertical needs likely looks more like project finance than venture equity: long-horizon, asset-backed, tied to infrastructure buildout.

Inclusive agri-fintech

The region has a $12-15 billion SME financing gap, and the models that are gaining traction have stopped trying to build distribution from scratch. New approaches are shifting from prohibitive “direct-to-farmer” lending toward trade-data underwriting, where transaction histories with established distributors become the basis for credit decisions.

By partnering with existing distribution networks rather than building their own, these platforms can achieve unit profitability through transaction fees and data monetisation. A related growth area is parametric insurance for aquaculture and livestock, which the report identifies as a billion-dollar opportunity, building on the climate adaptation demand outlined above.

The test for whether an emerging market agritech model will work is whether it can reach customers through infrastructure that already exists, or whether it needs to build the infrastructure first. The models gaining traction in SEASA are built on what is already there.

Of the three verticals here, agri-fintech is probably the one most naturally suited to standard venture capital: it runs on existing distribution rails, generates transaction-level data from day one, and can reach unit profitability without building physical infrastructure.

Sustainable feed and biotech

Sustainable inputs like algae and insect protein are attracting investment driven by clear demand from feed mills across the region. In the Philippines, aquaculture biotech ventures are integrating upstream solutions (the biology) with downstream brand partnerships (the market access).

With feed as the dominant cost driver across aquaculture species, alternative protein inputs are being pulled by the sector’s own cost structure. This is demand-led innovation, not supply-pushed technology looking for a market. And the capital structure follows the demand: corporate VCs from feed mills and processors (Thai Union Ventures, CP Group, Wilmar) are the natural funders here, because they are also the customers. This is perhaps the vertical that has the strongest set of acquirers.

Corporate acquisitions at $200-400M are the market revealing what works

If the first wave’s capital model was wrong, what does the right one look like? The exit data is a good place to start, because exit architecture tells you what the market rewards.

Since 2020, corporate acquisitions have accounted for roughly three-quarters of all SEASA agritech exits. Only eight IPOs have been completed across the broader ecosystem. The realistic exit target is $200-400 million, driven primarily by strategic buyers like Wilmar, Thai Union, and CP Group looking to de-risk supply chains and accelerate digital transformation.

This tracks with a pattern I covered in Issue #137 on the Verdant M&A review: thesis-driven corporate buyers are replacing conglomerate logic as the primary acquirers in food and agriculture globally. In SEASA, the same dynamic plays out with regional corporates filling specific platform gaps.

And exit proceeds are rarely recycled into new funds, creating what the report calls a “single-use” dynamic: without successful exits cycling capital back, new money must constantly flow in, compounding liquidity constraints across the ecosystem.

Niche exit pathways are also emerging. In India, SME listing platforms like the Bombay Stock Exchange SME have provided liquidity for smaller ventures with post-issue paid-up capital as low as $3-$4 million.

From my experience in the region, interest in secondary transactions is also picking up as early investors look for liquidity without waiting for a full exit. This is a global trend: as Cyril Ebersweiler, General Partner at SOSV, a global deep tech venture firm, shared in our conversation, secondaries grew from 10% to 28% of exit volume globally between 2020 and 2024, capturing 71% of exit dollars in 2024. If that trend reaches SEASA, it could ease the “single-use” capital constraint that currently starves the ecosystem of recycled capital.

Blended finance is the right architecture, with caveats

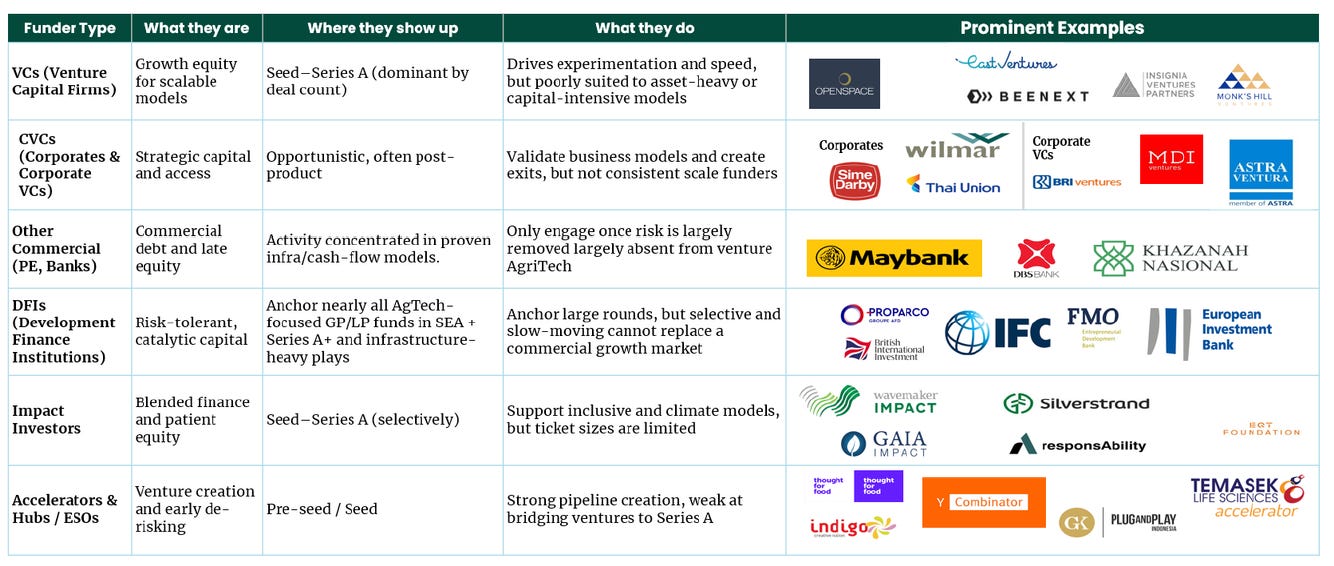

On the capital side, the architecture replacing VC primacy is blended finance: equity combined with credit and concessional capital. DFIs like the IFC, FMO, and Rabo Foundation are emerging as critical anchors, acting as cornerstone LPs in most newly launched agrifood funds with a combined $650 million committed to date.

Local financial institutions now participate in over a quarter of corporate-backed agritech deals, blending equity with working capital or ecosystem lending. Corporate VCs are the second-leading investor type after traditional VCs, providing both capital and the market validation that a business solves a real problem for a buyer.

Companies that have revenue profiles supporting debt instruments are increasingly raising capital through non-equity channels. The capital stack is diversifying because it has to. As Oscar Ramos, Managing General Partner at Orbit Ventures, an emerging-markets venture platform, mentioned in our conversation, designing a capital stack that matches the realities of the business is becoming just as important as designing the product itself.

A note of transparency: this report was commissioned by Omnivore, FMO, IFC, and Rabo Foundation, all of whom operate within the blended finance and impact investing model the report advocates. That doesn’t invalidate the analysis, the data is rigorous, and the findings track with what I see in practice. But you should hold the report’s enthusiasm for blended finance with an awareness that its commissioners have a structural interest in that architecture succeeding.

And on that point, while I am all for blended finance, I want to caution that blended finance is not as clean a solution as it sounds on paper. The trade-offs are real, and founders need to understand them.

The first is speed. DFI capital comes with decision timelines that can stretch months longer than commercial rounds. A startup competing for a distribution partnership or reacting to a regulatory window may not have that time.

The second is flexibility. Impact mandates can directly conflict with the pivots that startups need to make to survive. Consider an alternative protein startup backed by concessional capital tied to plant-based or fermentation-derived outcomes. If that company discovers its fastest path to unit economics runs through a partnership with an animal-based protein processor (co-manufacturing, shared cold chain, blended product lines), that pivot may be incompatible with the terms of its funding.

Blended finance is the right structural direction for SEASA. But the cost is flexibility and speed, and in markets where conditions shift fast, those can add up.

What I’m taking away from this

Build for acquisition readiness from the start

In a market where three-quarters of exits are corporate acquisitions in the $200 to $400 million range, the exit strategy is a founding thesis decision, not a Series B conversation.

The diagnostic questions for founders: Which three to five corporates are the most likely acquirers for your specific capability? Are you building something that slots into their workflows, or something that requires them to change how they operate?

And critically: don’t “go regional” until your local ecosystem can sustain the growth. The Series C Trap is a sequencing problem, and the sequencing starts at founding.

Fund architecture must match exit architecture

If the exit ceiling is $200 to $400 million, the fund math dictates everything downstream. A fund sized in that range can underwrite to these exits and generate meaningful returns at reasonable ownership levels.

A $200 million-plus fund requires a fundamentally different portfolio construction to make the math work, perhaps through multi-stage reserves, or a hybrid equity-credit model. The question for LPs: are fund sizes being calibrated to the market's exit architecture, or to LP appetite for larger commitments?

For investors building emerging market theses beyond SEASA

The structural conditions that make standard VC architecture a poor fit for SEASA (fragmented local markets, smallholder dominance, compliance-driven demand, infrastructure gaps that precede software adoption) exist in Sub-Saharan Africa, parts of Latin America, and Central Asia.

The SEASA correction is a dataset on what happens when capital architecture is imported rather than designed locally. The fund structures, check sizes, and exit expectations that emerge over the next two to three years will become templates, both for what to replicate and what to avoid.

If you found value in this newsletter, consider sharing it with a friend who might benefit from it!

Or, if someone forwarded this to you, consider subscribing.

Disclaimer: The views and opinions expressed in this newsletter are my own and do not reflect those of my employer, affiliates, or any organisations I am associated with.

Really liked this. It actually connects quite well with something we touched on in our Novonesis piece too: a solution can have clear value on paper, but that still does not mean adoption will be easy or fast.

In the end, it still comes down to things like distribution, local incentives, regulation, and whether the market is actually ready for it. That part often looks a lot simpler in the story than it is in real life.

Appreciate the added analysis and perspectives you had on the report.