$13M for Full-Stack Fermentation, and $10M to Rewire Plant Immunity

Also: China is about to do to global agriculture what it did to solar and EVs.

Hey there!

Welcome to the 146th edition of Better Bioeconomy, insights on startups, capital, and ideas reshaping food and agriculture for better human and planetary health.

Below, I have curated the 10 most interesting agrifood tech stories I came across last week, paired with my thoughts on what they mean for where the industry is heading.

This week’s edition covers livestock data infrastructure, methane-cutting feed tech, plant immunity platforms, precision fermentation, cocoa-free chocolate, and China’s industrial play on global food.

🧬 StrainX Bioworks emerged from stealth with $13M to scale precision fermentation ingredients for food and nutrition

The India-based startup runs a 10,000-litre facility and 100+ team, with modular capacity that scales toward 100,000 litres over the next 12-18 months as commercialisation lines up. Specific ingredients remain undisclosed, though initial work is in alt proteins.

StrainX takes a full-stack approach, building strain engineering, process development, fermentation scale-up, downstream processing, and manufacturing in-house rather than relying on co-manufacturers. The startup says India offers limited precision fermentation infrastructure outside pharma, so owning the stack lets it control process economics and iteration cycles.

One molecule has self-affirmed GRAS status in the US with a no-questions letter pending, and multiple ingredients are awaiting Indian approval. StrainX claims price parity with conventional versions, helped by what it calls structural manufacturing advantages in India, and is positioning as a B2B partner to global food and ingredient companies.

Investors: Prime Venture Partners, Leo Capital, Good Startup, Sparrow Capital, Sun Icon Ventures, Dholakia Ventures, WindT Angels

Source: Green Queen

Thoughts 🤔

The full-stack framing in StrainX’s round is doing a lot of work. They call internal manufacturing a strategic choice for owning process knowledge and long-term defensibility, which is a real moat argument.

But India’s food-grade precision fermentation CMO infrastructure is still coming together outside pharma, so building strain engineering, downstreaming, plant operations, and commercialisation in-house was also the only path to 10,000-litre scale. Both can be true.

The harder question is what that combination costs to defend. StrainX is carrying the entire stack plus a 100-person team on a single Series A, while Western peers raising similar tickets stay asset-light through contract capacity and route burn into strain work and customer development. Whether full-stack compounds into defensibility or becomes a CAPEX overhang depends on how quickly the Indian CMO layer matures around them.

🌱 Resurrect Bio closed its Series A at $10.3M to restore crops’ natural disease defences through gene-editing targets

The UK startup, spun out of The Sainsbury Laboratory in Norwich, identifies how pathogens suppress plant immunity and pinpoints the edits needed to switch defences back on. The round follows an $8.1M initial close in February.

Plants rely on NLR immune receptors to fight off threats, but pathogens secrete effector proteins that bind to these receptors and shut down the response. Resurrect Bio’s FloraFold AI predicts those protein-protein interactions and screens them in-silico and in-planta, then hands seed company partners the exact gene-editing template to break the binding.

The funds scale the team and develop resistance traits in major crops, building on a joint development agreement with Corteva in corn. The model sidesteps chemical inputs and works across most crops, pathogens, and pests, opening room for more deals with seed companies and breeders.

Investors: Corteva Catalyst, Calculus Capital, Pymwymic, Future Planet Capital (UKI2S), SynBioVen, AgFunder

Source: AgFunderNews

Thoughts 🤔

Corteva Catalyst has now made ~6 biology-first bets in twelve months, spanning microbes, peptides, AI proteins, and plant immunity. Resurrect Bio is the latest. The cadence and breadth point toward a distributed external R&D function rather than discrete corporate venture activity.

Synthetic crop protection registration costs have crossed $300M with 12-year timelines, regulatory windows are narrowing, and pathogen resistance is eroding existing chemistry. Catalyst lets Corteva access biological mode-of-action innovation through joint development agreements and pre-negotiated licensing options, without carrying internal R&D overhead.

This could be the template for how big ag runs R&D for the rest of the decade. If it does, value accrues to platform companies with optionality across incumbents, not to those who go exclusive early. The tell will be how many of these six investments convert to exclusivity over the next 18-24 months.

🐄 URUS acquired AgriWebb to bring integrated data infrastructure to the global beef industry

The Australian livestock management platform collects field and cowshed data for farm mapping, grazing, and inventory tracking across 10,000+ farms, 23 million animals, and 150 million acres in 26 countries. It also acts as supply chain infrastructure for McDonald's, Nestle Purina, Wendy's, Ahold Delhaize, and Sainsbury's.

URUS runs nine brands across dairy and beef genetics, reproductive services, and dairy software. AgriWebb pushes the platform to 25 million animals and extends URUS’s dairy flywheel into beef, linking breeding, animal health, sustainability, and traceability in one system.

The deal reflects a wider structural shift: livestock technology is moving away from standalone tools toward integrated systems connecting genetics, animal health, environmental data, and supply chain traceability into something that functions more like critical infrastructure.

Source: AgFunderNews

Thoughts 🤔

URUS already runs a genetics-data flywheel in dairy through VAS and DairyComp, where individual-animal monitoring feeds back into which semen gets sold next. Beef has historically broken that loop because grazing systems are extensive and data-poor. Building telemetry across 10,000 farms in 26 countries is a 10-15 year capital problem, so URUS bought the instrumentation layer instead of building it.

The genetics-as-platform frame also reframes what AgriWebb is worth to this specific buyer. Standalone, it's livestock SaaS with thin comparables. Inside URUS, it's the input layer that lets dairy-style genetics decisions extend into beef, where AI penetration has plateaued and Scope 3 buyers are creating new demand for producer data.

🍫 California Cultured and UC Davis won $2.8M in US government grants to cut the cost of cell-cultured chocolate

The California startup is working with UC Davis to scale its cultured cocoa platform, with commercial manufacturing slated for early 2027 to fulfil a first purchase order. The grants from BioMade and NSF are part of a 14-project DoD-backed push to strengthen domestic biomanufacturing.

Current cellular agriculture economics for cocoa are punishing, with steel bioreactors, high-pressure steam sterilisation, and low batch productivity all driving up operating costs. The team will design custom high-density polyethylene (HDPE) bubble bioreactors, test alternative sanitisation strategies, and run semi-continuous operations with real-time in-line biomass monitoring to lift volumetric productivity.

Internal tests show the HDPE reactors outperforming stainless steel in plant cell culture. The work also feeds into low-cost drying, food-safe media, and strain productivity, with techno-economic and life-cycle analyses to test transferability across plant, algal, microbial, and fungal systems.

Source: Green Queen

🧫 Melazyme raised $2M seed to advance precision-fermented melanin and sweet proteins platform

Founded in 2025 by two Perfect Day alums, the US startup uses precision fermentation to make biomolecules, led by melanin. It engineers strains for high-yield melanin synthesis on renewable carbon feedstocks and uses solvent-free purification to yield a powder it calls Black Gold.

Melazyme claims its melanin reaches >99% purity, well above the 70-80% from cuttlefish-extracted melanin and the 75% of chemically synthesised versions. The naturally occurring biopolymer combines broad-spectrum UV absorption, chemical stability, and strong affinity for metal ions, opening applications across cosmetics, functional coatings, filtration, and rare-earth element recovery.

Near-term commercial focus is cosmetics, where Melazyme is engaging global manufacturers and has developed a melanin precursor that binds to hair keratin to restore colour without ammonia or oxidative dyes. It has also advanced brazzein, a heat-stable sweet protein from the West African Oubli fruit, 500-2,000x sweeter than sucrose, with commercial partners.

Investors: SeaX Ventures, Stellaris Venture Partners, Plug and Play Ventures

Source: Green Queen

Thoughts 🤔

The melanin-cosmetics framing makes Melazyme look like a category pioneer, but from my light research, it is the second venture-backed entrant on this molecule. IndieBio-backed Avisa Myko has been at it since 2019 on a cost-collapse pitch, claiming $0.20/gram melanin versus a $400/gram reference.

Melazyme is going the other way, leading with 99% purity versus 70-80% for cuttlefish-extracted and 75% for chemical synthesis. My read is that this is less a head-to-head and more a category bifurcation. Cost wins mass-market sunscreen and PPD-free hair dye. Purity wins premium cosmetics and any medical adjacency.

Separately, I would treat the brazzein side of the platform as narrative more than commercial intent. If they do get into the brazzein market, Melazyme is entering one of the most over-crowded subcategories in precision fermentation. If there is no GRAS pathway disclosed within 12-18 months, I’d treat brazzein as platform decoration and assume the real business is melanin.

🐄 Triple Bio raised €1.5M to advance lipid-based feed additive platform to cut methane and boost milk yields in dairy cattle

The Netherlands-based startup runs two lipid formulations. RumeNRG-PL encapsulates existing methane inhibitors like bromoform, protecting actives from rumen degradation and enabling gradual release. RumeNRG-Mx1 is a standalone additive that redirects hydrogen flow in the rumen without any loaded compound.

Rather than suppressing methanogens, the approach makes hydrogen more bioavailable to fermentative bacteria that generate most of the animal’s metabolic energy. In vitro rumen simulations showed a 28% boost in volatile fatty acid production, which Triple Bio says could mean 5-10% higher milk yield. The encapsulated formulation also matches methane reduction at 500x lower dose.

Live-animal trials run later this year, with proof-of-concept data feeding a larger 2026 round. The longer-term ambition: one product line delivering productivity gains and up to 50% methane reduction without any loaded inhibitor.

Investors: Nucleus Capital, Positron Ventures, Climate Club

Source: AgFunderNews

Thoughts 🤔

Triple Bio’s near-term product is aimed at the companies already in enteric methane sitting on stabilisation, dosing, and palatability problems with their own actives. A 500-fold dose reduction on a known inhibitor is a margin gift to Rumin8, Symbrosia, and the bromoform/3-NOP cohort, not a competitor.

The split mirrors how pharma separated APIs from formulation once actives cleared regulatory and delivery became the next defensible layer. Rumin8 patented oil-based stabilisation for tribromomethane. DSM spent over a decade taking 3-NOP through EFSA and FDA. With the molecules now squeezed by dose-related cost, safety thresholds, and consumer backlash, encapsulation is where competitive economics are won, and the actives commoditise underneath.

🤝 Endless Food Co lands Dagrofa deal to push bean-free chocolate into Danish foodservice

Denmark’s Endless Food Co has signed a strategic partnership with Dagrofa Foodservice, one of the country’s leading foodservice distributors, to get its cocoa-free chocolate alternative THIC (This Isn’t Chocolate) into professional kitchens nationwide.

THIC is built from upcycled side streams, including brewer’s spent grain, cacao husks, and oat milk pulp, which make up to 40% of the product. The rest is wild-harvested shea butter and organic beet sugar, processed through traditional chocolate-making into a powder that drops into existing production lines.

The deal opens a major new commercial channel for the startup as cocoa prices remain under sustained pressure from climate-driven supply shocks. It also follows the company’s earlier retail push with 7-Eleven Denmark, signalling a parallel build across foodservice and convenience retail.

Source: Green Queen

Thoughts 🤔

The cocoa-free chocolate story has been written mostly through retail and industrial confectionery rails. Barry Callebaut-Planet A Foods, Cargill-Voyage Foods, Mars and Nestlé picking up ChoViva. Endless Food Co’s Dagrofa deal opens a different rail and one I suspect is underrated. Dagrofa is Denmark’s market leader in canteens and hotels, runs ~35,000 SKUs across a nationwide fleet, and already supplies Compass Group’s roughly 100,000 daily meals in the country.

Institutional foodservice is a structurally different buyer to retail confectionery. Procurement turns on cost per kg, batch consistency, supplier reliability, and operator ease. The channel is slower to enter but stickier once in, and largely insulated from the retail cycle driving most cocoa-free coverage.

🥟 Intake unveiled Takein to push precision-fermented yeast protein and fibre into global B2B supply

Takein is the new ingredient arm for the South Korean startup’s precision-fermented yeast protein and fibre, marking its shift into a ‘materials-focused’ model ahead of an IPO. The launch comes a year after Intake’s $9.2M Series C to scale its grape-derived wild yeast strain.

The yeast protein isolate is positioned as a third-generation whey replacement, with a complete amino acid profile and what the company claims are higher digestion and absorption rates and lower allergy risk than dairy whey. The yeast-derived fibre is extracted from the cell walls left after protein fractionation and contains beta-glucan and mannose, which Intake says support immune function and gut health.

Intake will trial commercial use through its own brands first, ProteeOne protein powders and Sugarlolo’s sugar-free range, before scaling supply to global manufacturers.

Source: Green Queen

🧫 Capra Biosciences cut fermentation monitoring costs with chickpea-sized wireless biosensors floating inside its bioreactors

The Virginia-based startup, which makes retinol and other high-value ingredients via biomanufacturing, is partnering with Boston University on a wireless network of free-floating microbial-electronic sensors that pair engineered light-emitting cells with embedded electronics. Backed by NSF and BioMADE, the sensors will be miniaturised and tested at Capra's 10,000 sq ft pilot facility.

Traditional pH, dissolved oxygen, and CO2 probes cost $5,000-$10,000 each, require insertion into the broth, risk contamination, and give a single-point view. Capra says the new biosensors could hit $10-$100 per unit at scale, measure multiple analytes through an onboard potentiostat, and float at different points for spatial visibility.

The economics matter most for Capra’s modular setup, which runs multiple 1,000-L units rather than one large tank and could eventually involve hundreds or thousands of reactors per facility, making sensor cost a material driver of unit economics. The company has also just launched what it claims is the first fermentation-derived salicylic acid for personal care, and says it has run continuous production of that molecule for up to 100 days.

Source: AgFunderNews

Thoughts 🤔

The Capra biosensor story is being framed as a cost story. I think the more interesting frame is what free-floating sensors enable. Industrial fermenters are full of gradients. Oxygen, pH, substrate, and shear all vary across the vessel, and current control systems essentially ignore that because they can’t see it.

One probe near the wall is treated as a fair proxy for a well-mixed tank that may not really exist at scale. The mainstream workaround has been mechanistic CFD modelling and more aggressive mixing, both of which hit physical and energy limits as reactors grow.

A wireless network of free-floating sensors changes the data substrate. It gives spatially distributed, time-resolved readings of pH, dissolved oxygen, redox state, and bioluminescent stress signals from engineered Yarrowia lipolytica reporters across the broth. That is the missing input layer for the AI-driven fermentation control everyone has been pitching but few has had the data to actually train.

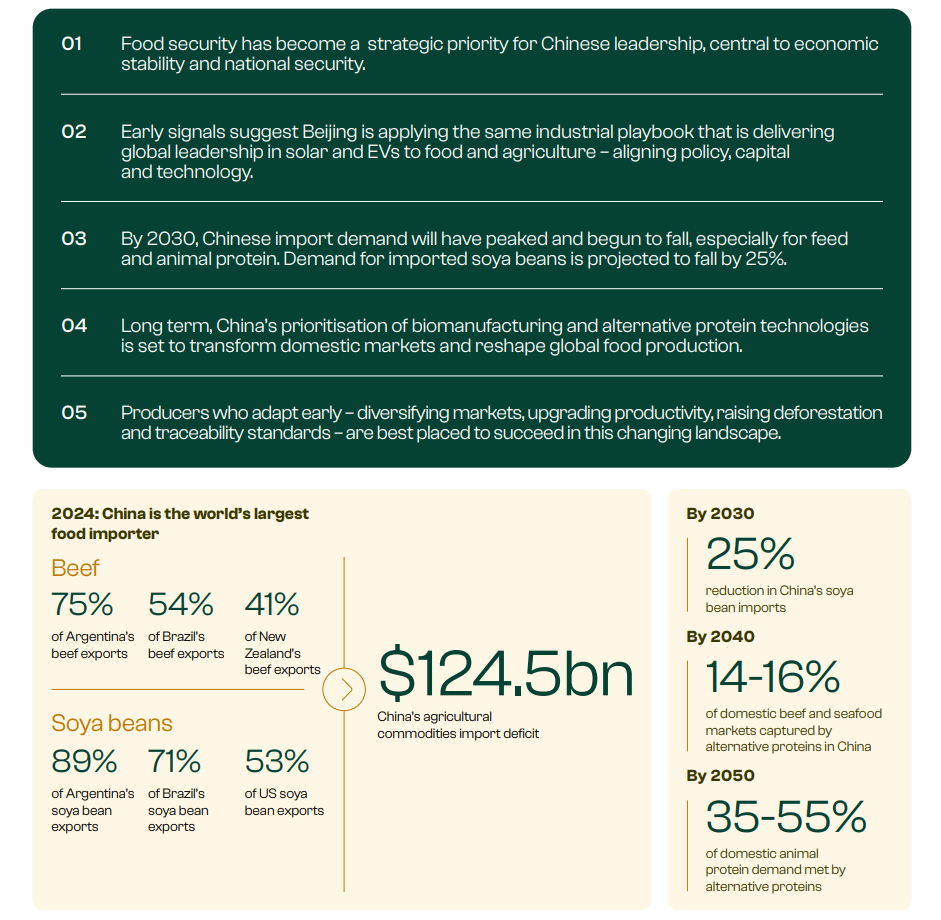

🇨🇳 Report: China is about to do to global agriculture what it did to solar and EVs

Beijing is applying the same industrial playbook behind its dominance in solar, wind and EVs to food and agriculture. The 14th Five-Year Plan was the first to place food security alongside energy and finance as a pillar of economic security, and the 15th explicitly bets on synthetic biology, alt proteins and agricultural biotech. Commercialised GE maize and soya approvals in 2024 signal the policy machinery has switched on.

By 2030, China’s soya bean imports are projected to fall by 23.5 million tonnes, a 25% drop worth roughly $12 billion. That is almost equal to everything the US shipped to China in 2024. Smaller contractions hit beef, poultry, dairy and egg imports, driven by feed reformulation, a 50% cut in avoidable food loss, and productivity gains on existing land.

By 2040, the report projects China will flip to a net exporter across poultry, dairy, eggs and farmed aquatic products, with alt proteins already taking 14% of beef and 16% of seafood domestically. Producers in those categories will face Chinese exports in their home markets, on top of losing the buyer they were built to serve.

The report models alt proteins meeting 35-55% of Chinese animal protein demand by 2050, with cultivated meat commercially viable in the 2040s. More importantly, it argues that China captures the upstream value chain, amino acids, fermentation infrastructure, and bioreactor supply, replicating its position in solar wafers and lithium cells.

Exposure is concentrated. China absorbs 89% of Argentina’s soya exports, 71% of Brazil’s and 53% of the US’s, plus 75%, 54% and 41% of Argentine, Brazilian and New Zealand beef. Producers who move first on deforestation-free supply, traceability and market diversification will manage the transition. Those who don’t face simultaneous volume and price contractions.

Source: Systemiq

CAPITAL & CONVICTION

The sharpest thinking in agrifood and bioeconomy often happens off the record. My interview series brings it on the record:

Why 2026 Is the Great Shakeout Year for Food and Ag Tech - EcoTech Capital’s Adam Bergman

What It Takes to Build a Fundable Food Company After “Peak Stupid” - Siddhi Capital’s Steven Finn

Engineering the Exit: How to Get Acquired in Deep Tech - SOSV’s Cyril Ebersweiler

Turning the Industrial Biomanufacturing Graveyard Into a Winning Playbook - First Bight Ventures’ Veronica Breckenridge

How Agrifood Tech Investing Is Shifting and Where Value Will Be Created - PeakBridge’s Yoni Glickman

Browse the full archive. More conversations dropping soon. Stay tuned!

Thanks for reading!

Let me know your thoughts in the comments or by replying to this email. If you want to connect with me on LinkedIn, you can find me here.

If you found value in this newsletter, consider sharing it with a friend who might benefit! Or, if someone forwarded this to you, consider subscribing.

Disclaimer: The views and opinions expressed in this newsletter are my own and do not necessarily reflect those of my employer, affiliates, or any organisations I am associated with.