$533M Doing What Ag Tech VCs Won't

Also: $24M for precision-fermented dyes ahead of the synthetic ban, Infinite Roots buys Bosque, and China’s first open-source AI model for crop protection

Hey there!

Welcome to Issue #147 of Better Bioeconomy, insights on startups, capital, and ideas reshaping food and agriculture for better human and planetary health. Thanks for being here.

Below, I have curated the 10 most interesting agrifood tech stories I came across last week, paired with my thoughts on what they mean for where the industry is heading.

This week covers natural food colours ahead of the Red No. 3 cliff, mycelium meat on brewery infrastructure, compliance-aware crop AI from China, post-bankruptcy precision fermentation playbooks, philanthropic capital filling the agtech valley of death, and virtual fencing’s US land grab.

🎨 Phytolon raised $23.6M Series B to commercialise its yeast-fermented beetroot red dye in the US

The Israeli startup uses precision fermentation of baker’s yeast to produce natural pigments for food, replacing petroleum-based synthetics like Red Dye No. 3 and Red 40. Its platform is built on two core pigments, yellow and purple, which can be blended into a palette spanning yellow, orange, pink, purple, and red.

Phytolon genetically engineers yeast to express betanin, the water-soluble pigment found in red beets, then strips the production organism from the fermentation broth. The resulting colourant is heat- and pH-stable, comes in liquid and powder formats, and works across bakery, savoury, frozen, dairy, and confectionery.

The round closed in three stages, with the majority of capital landing in April. Funds will go toward sales, supply, and distribution partnerships in the US, where the FDA cleared beetroot red in February and simultaneously allowed “no artificial colors” labelling for products free of petroleum-based dyes. A prickly pear yellow is next in the pipeline.

Investors: Millennium Foodtech, NextGen Nutrition, Colorcon Ventures, Yossi Ackerman, and an undisclosed strategic investor

Source: Green Queen

Thoughts 🤔

Phytolon’s Series B sits on two structural conditions. The first is a deadline-driven buyer market. Red No. 3 exits the food supply by January 2027, with HHS/FDA pushing the other six petroleum dyes out by end of 2026.

For CPG procurement teams, that converts natural colour adoption from a clean-label preference into a fixed-date reformulation event. Phytolon’s February 2026 FDA clearance puts it 11 months ahead of the cliff while some startups are still in submission, and the next 18 months of contract pricing power look structurally stronger than the standalone unit economics would suggest.

The second condition is what the round reveals about food ingredient capital. A Series B closing in three tranches, with the majority landing in April from an undisclosed strategic, is staged commitment rather than a single-close conviction round, even with regulatory clearance and a deadline-driven buyer base behind it. My read is that this is what “good” precision fermentation rounds look like now: milestone-gated capital, strategic underwriters, and investors monitoring performance before deploying the full cheque. Founders in the category should plan around staged closes rather than single dates.

🍄 Infinite Roots acquired Bosque Foods to expand its mycelium meat portfolio

The Hamburg-based biotech picked up the Berlin-founded startup for an undisclosed sum, nearly two years after Bosque liquidated its subsidiary following regulatory hurdles in the EU. The deal folds Bosque’s whole-cut chicken, pork filets, and bacon into Infinite Roots’ mycelium protein lineup.

Infinite Roots runs submerged fermentation, growing edible mushroom strains in steel tanks on a nutrient-rich broth. Bosque uses solid-state fermentation, growing microbes on inoculated solid surfaces fed by low-value agrifood sidestreams. Combining the two methods gives Infinite Roots both scale and structured whole-cut formats from one platform.

The acquisition adds Bosque’s IP, process data, and product knowledge to Infinite Roots’ industrial base, which the company says will speed scale-up and broaden its format range.

Source: Green Queen

Thoughts 🤔

This looks like a tidy mycelium consolidation story, and the tech synergies are real with few mycelium companies owning both. What interests me more is the sequencing. Infinite Roots has rescinded its FDA GRAS filing to update its safety dossier, has no near-term EU novel food path, and rerouted commercial activity through South Korea via Pulmuone. Bosque faced the same EU bottleneck and now operates only out of New York. The acquirer is buying capability before clearing its own regulatory bar.

Most consolidation waves see survivors roll up distressed assets after the gating constraint is solved. Here, the regulator is the gating constraint, and the lengthy EFSA approval window means the 2022-2023 cohort was always going to hit a capital wall before approval.

My thinking is that this works if the updated US dossier lands GRAS in the next 12-18 months and EFSA’s reforms open the EU window in time for whole-cut formats. If neither moves, the process synergy still buys optionality wherever approval lands first, but two regulatory-stalled assets end up sharing one runway.

🍗 Pacifico Biolabs raised €7M Series A to brew mycelium chicken in beer tanks

The Germany-based startup uses fermentation to grow whole-cut mycelium meat, turning the microbes into a protein-rich biomass that mimics whole-muscle texture. It has pivoted from its original seafood focus to chicken, which it will sell to B2B clients under the Viando label and target supermarket shelves across Germany, Austria, Switzerland and the Nordics by late 2026.

Pacifico’s process runs in standard beer brewery tanks rather than purpose-built bioreactors, and the startup claims this cuts CAPEX by >95% vs traditional biomass fermentation routes. The approach works because the EU’s beer production has declined for 5 consecutive years, leaving fermentation capacity sitting idle and available for retrofit.

Funds will scale production to 200 tonnes/month in Saxony, expand the team, and lock in commercial partnerships ahead of the late-2026 launch. Pork and seafood formulations remain in the pipeline.

Investors: Stray Dog Capital, TGFS, Sprout & About Ventures, Simon Capital, FoodLabs, and a regional brewery partner

Source: Green Queen

Thoughts 🤔

Two German mycelium startups are now anchoring production on idle brewery infrastructure rather than purpose-built bioreactors. Infinite Roots has been doing the same, partnering with contract manufacturers and repurposing brewery sites on the same logic.

The timing fits the funding market. Purpose-built bioreactor plants priced in the tens of millions are uninvestable right now. Brewery retrofits compress the headline CAPEX number into something a Series A can handle.

That lowers the bar for the whole category to reach commercial scale without raising money the market won’t provide. The vessel is shared, but strain IP, fermentation process, downstream, and product quality still have room to differentiate.

🤝 BioPrime AgriSolutions and Mosaic team up to embed biologicals into mainstream fertilisers

The Pune-based ag biologics startup will plug its SNIPR-platform biologicals into Mosaic’s potash and phosphate fertiliser lines, with the companies pitching the joint offering as a “Crop Performance System” that goes beyond basic plant nutrition to support crops across the growth cycle.

The deal gives BioPrime a route into one of the world’s largest fertiliser distribution footprints. Mosaic supplies customers in more than 40 countries, so even modest attach rates on its volumes would put SNIPR-derived biologicals in front of growers at a scale most ag-biotech startups spend years trying to reach.

The companies say the integrated product is designed to improve return on crop nutrition spend and lift output from existing farmland without a matching rise in environmental impact. The framing matches where the industry is heading as fertiliser prices swing on geopolitical disruption and regulators push for lower-footprint productivity.

Source: AgroPages

🐄 Monil raised $10M to enter the US virtual fencing market

The Norway-based startup makes solar-powered cattle collars that create virtual boundaries for grazing herds. Monil has sold 50,000 collars across Norway, Sweden, and the UK since launching in 2022 and grew revenue 5x last year to $6.6M.

Beyond fencing, the collars track activity to flag entrapments and illness, and the startup is now layering on reproductive monitoring. Heat detection launched in May using rumination data, with calving detection arriving in autumn based on other activity signals.

The capital funds a US launch from a new Kansas City base, where Monil is recruiting sales and field staff and has completed regulatory prep. The company says it is ready to ship to the American market and views the US as a growing opportunity with rapid developments underway.

Investors: Firda and other Norwegian venture capital investors

Source: Beef Magazine

Thoughts 🤔

Halter raised $220M recently and now spans 200+ ranches in 22 states. Vence sits inside Merck Animal Health on 4M acres. Gallagher’s eShepherd has been live in North America since 2024 with existing ag retailer relationships.

Monil is entering at much smaller scale against entrenched competitors. I am curious to see how Monil carves out a defensible position. The Kansas City base hints at a cow-calf focus rather than Western rangeland, where the big three concentrate. Whether Nordic product economics hold for US operators is the other open question.

🌾 Nanjing Agricultural University unveiled China’s first open-source AI model for crop protection

Called Green Shield, the model was built by NAU’s College of Plant Protection with the National Key Laboratory of Agricultural Biosafety and 30+ industry institutions. It was trained on 2.5B tokens from academic papers, patents, national standards, and field reports spanning rice, wheat, soybeans, vegetables, and fruit trees.

Green Shield identifies crop type, growth stage, and disease symptoms to generate integrated pest management strategies. Before any recommendation, it cross-checks proposed chemicals against China’s national pesticide registration database, blocking non-compliant suggestions on banned substances, approved crop applications, or dosage limits.

The release follows Sinong, NAU’s general agriculture LLM trained on 4B+ tokens and shipped in 8B and 32B versions earlier this year. Together they give Chinese agriculture a specialised open-source AI stack, from broad agronomic guidance to compliance-aware crop protection advice in a country where pesticide misuse and resistance remain persistent grassroots problems.

Source: iGrow News

Thoughts 🤔

A free, compliance-grounded crop protection advisor inside the world’s largest pesticide market could change how this layer gets monetised. In my view, tools like Climate FieldView and Cropwise have never really sold standalone advisory revenue per user. They are loyalty layers designed to pull through branded seed and chemistry. Green Shield’s threat is margin pressure on the chemistry book, since a neutral recommender could nudge farmers toward generic actives over branded portfolios.

China’s economics were already hostile to paid advisory products for smallholders, though mid-scale cooperatives and new-type operators do pay for advisory tooling. Open-sourcing a compliance-aware model removes whatever pricing power sat in the model layer.

If Green Shield holds up in deployment, value likely accrues to the players already touching farmer transactions, like input retailers and platform players, rather than the input majors defending branded chemistry through digital agronomy.

🎢 Amyris CEO on re-emerging from bankruptcy with a leaner model built on recurring revenue

Two years after its 2023 Chapter 11 filing, the synthetic biology pioneer is operating with a monthly burn rate that the company says matches what it used to spend in a single month under prior management. CEO Kathy Fortmann says Amyris closed 2025 a year ahead of plan on both top and bottom lines, though the company is not yet profitable.

Amyris has exited consumer brands, shed unfavourable contracts, and returned to its roots as a B2B biotech. The company is prioritising recurring revenue from licensing and royalties over large upfront partner payments, and applying back-of-envelope economics earlier to avoid burning cash on molecules that won’t pencil at scale.

Fortmann has also broken the rule that every collaboration ends with Amyris manufacturing the ingredient. The company will now do strain engineering and process development for partners and license the output, reserving its precision fermentation plant for specialty molecules. Ag biologicals is a new focus, with Amyris targeting startups and incumbents that need help with strain optimisation, scale-up, or initial manufacturing.

Source: AgFunder

Thoughts 🤔

A useful read for founders building in biomanufacturing on which layer of the stack is worth owning. The first wave of precision fermentation companies bet that the durable moat came from owning everything: strain, process, manufacturing, often the consumer brand on top. That thesis assumed cheap capital and patient timelines, and both have gone.

Amyris is the visible example of what happens when full-stack ambition runs into the cash discipline needed to make any single layer profitable. Ginkgo is converging on a similar narrower repositioning after its own restructuring. The survivors are picking the layer they want to own, monetising it through recurring revenue, and treating adjacent layers as someone else’s problem. The strategic question for the next cohort is no longer “what molecule” but “which layer”.

💰 Renaissance Philanthropy bets on “venture capital for public good” to reshape agricultural innovation

Renaissance Philanthropy has mobilised $533M across 22 programmes and five government partnerships, with $265M routed to third parties and $268M into internally managed initiatives. The two-year-old nonprofit pitches itself as a field builder, structuring thesis-driven programmes with stage-gated decision points more akin to venture studios.

Much of its agricultural work sits inside the Advanced Research for Climate Emergencies (ARC) fund, targeting underexplored risks like methane and nitrous oxide emissions, ag-driven deforestation, and climate tipping points. Through the Climate Emergencies Resilience Lab, built with Deep Science Ventures, it identifies scientific opportunities and spins up agtech ventures where commercial pathways exist.

The bet is that philanthropic capital can de-risk the agtech “valley of death” through 5-7 year programmes that produce decision-grade science and hand off to governments, corporates, or investors. Renaissance claims climate stabilisation receives <0.1% of global climate finance, framing agriculture as a node where risk-tolerant capital could unlock returns conventional funders can’t reach.

Source: AgNavigator

Thoughts 🤔

The “venture capital for public good” framing obscures the more interesting structural read. The operating model: 5-7 year programmes, milestone-gated, domain-expert-led, with handoff plans is closer to a Focused Research Organization than a venture studio. FROs have crowded into protein structure, brain connectomics, and climate measurement through folks like Convergent Research and Astera. But agriculture has been largely absent from that wave.

The gap they fill is the messy middle between USDA-style basic research, CGIAR-style smallholder programmes, and venture-backed agtech. None of those fund a 5-year team chasing a specific milestone in crop biology with a defined sunset and a public-good deliverable. FROs landing in agriculture now is a counter-cyclical move into a vacuum. The big ag players have pulled back internal R&D, USDA budgets are constrained, and CGIAR is in a funding crisis.

If Renaissance can scope milestones that produce shared infrastructure (phenotyping platforms, trait libraries, climate-response biological databases), the compounding leverage downstream could look closer to what AlphaFold gave structural biology than what venture has produced in ag tech.

🛡️Syngenta opens $10M Almería R&D hub to halve breeding timelines against fast-emerging crop pathogens

The R&D Technology Centre in El Ejido, Almería, consolidates breeding, trait development, seed operations, fruit quality, applied data science, and digital tools under one roof. Biosafety infrastructure on site lets researchers study high-risk pathogens in quarantine.

The location is strategic. Almería’s “Sea of Plastic” packs >30,000 hectares of greenhouses producing ~4M tonnes of vegetables annually, giving breeders constant, diverse disease pressure to stress-test varieties under commercial conditions. Syngenta says a new serious pathogen now emerges roughly every 2 years, with threats like ToBRFV and Downy Mildew driving the urgency.

The company claims the facility can cut breeding timelines by up to 50%, taking varieties from 4 years to as little as 2, on the back of AI and ML in its breeding pipelines. Insights generated locally feed Syngenta’s global R&D network, with the field-to-lab model designed to shorten the loop between pathogen identification and resistant seed delivery.

Source: AgNavigator

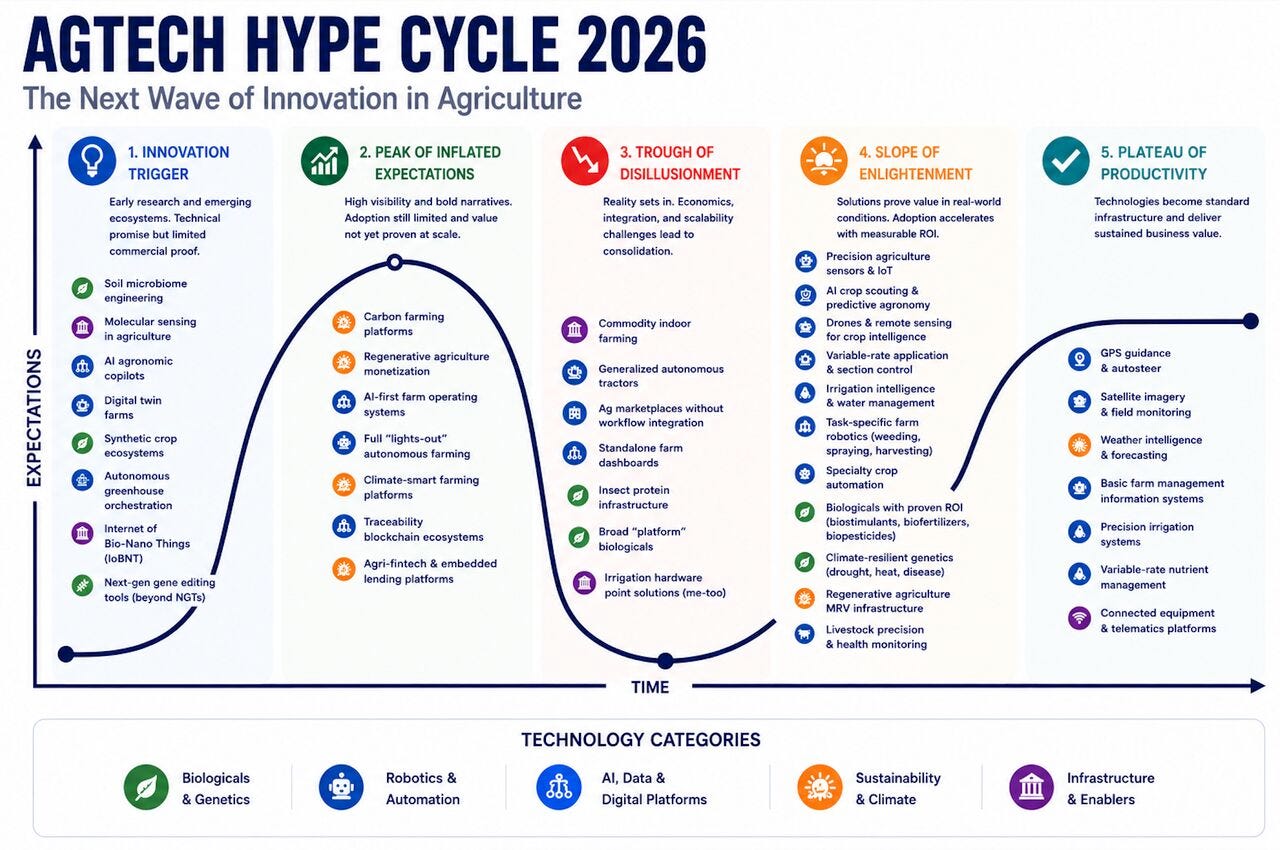

💭 Ag tech hype cycle 2026: The sector is entering its industrialisation phase

Hadar Sutovsky’s thesis is that value creation is shifting upstream into precision agriculture, irrigation intelligence, AI crop scouting, biologicals with proven ROI, and specialty-crop robotics. These categories are moving from experimentation into operational deployment, signalling AgTech’s transition from pilot purgatory to embedded infrastructure.

Hadar argues physical AI is becoming real on the farm through task-specific automation rather than the fully autonomous farm narrative that dominated earlier cycles. Biology is entering its execution phase too, with climate-resilient genetics, next-gen biologicals, and regenerative infrastructure now judged on field performance and integration into existing farm workflows.

The reset categories are indoor farming, generalised autonomy, and broad platform plays, all hitting the wall on unit economics, adoption friction, and infrastructure constraints. Winners will be the solutions that slot into systems farmers already use while delivering measurable ROI under real-world conditions.

Source: Hadar Sutovsky/LinkedIn

CAPITAL & CONVICTION

The sharpest thinking in agrifood tech often happens off the record. My interview series brings it on the record:

Why 2026 Is the Great Shakeout Year for Food and Ag Tech - EcoTech Capital’s Adam Bergman

What It Takes to Build a Fundable Food Company After “Peak Stupid” - Siddhi Capital’s Steven Finn

Engineering the Exit: How to Get Acquired in Deep Tech - SOSV’s Cyril Ebersweiler

Turning the Industrial Biomanufacturing Graveyard Into a Winning Playbook - First Bight Ventures’ Veronica Breckenridge

How Agrifood Tech Investing Is Shifting and Where Value Will Be Created - PeakBridge’s Yoni Glickman

Browse the full archive. More conversations dropping soon. Stay tuned!

Thanks for reading!

Let me know your thoughts in the comments or by replying to this email. If you want to connect with me on LinkedIn, you can find me here.

If you found value in this newsletter, consider sharing it with a friend who might benefit! Or, if someone forwarded this to you, consider subscribing.

Disclaimer: The views and opinions expressed in this newsletter are my own and do not necessarily reflect those of my employer, affiliates, or any organisations I am associated with.