$23M for Ag Knowledge AI Can't Skip, and $23M to Turn Eggs Into Biologics Factories

Also: Bayer's bioinsecticide deal with Aphea.Bio, Lacto Japan locks in Leaft's Rubisco protein, and Tate & Lyle widens its sweetener book weeks before a £2.7B sale.

Hey, it’s Eshan. Welcome to Issue #149 of Better Bioeconomy, insights on companies, capital, and ideas reshaping food, agriculture, and biomanufacturing for human and planetary health. Thanks for being here!

This week covers SWARM and Leaf, both betting that the operational and data layer beats the model, Aphea.Bio’s bioinsecticide deal with Bayer, Tate & Lyle widening its plant-cell sweetener work just before its Ingredion takeover, Neion Bio turning eggs into biologics factories, and the case for biomanufacturing as strategic infrastructure.

Below are the 10 most interesting ag and food tech stories I came across last week, paired with my thoughts on what they mean for where the industry is heading.

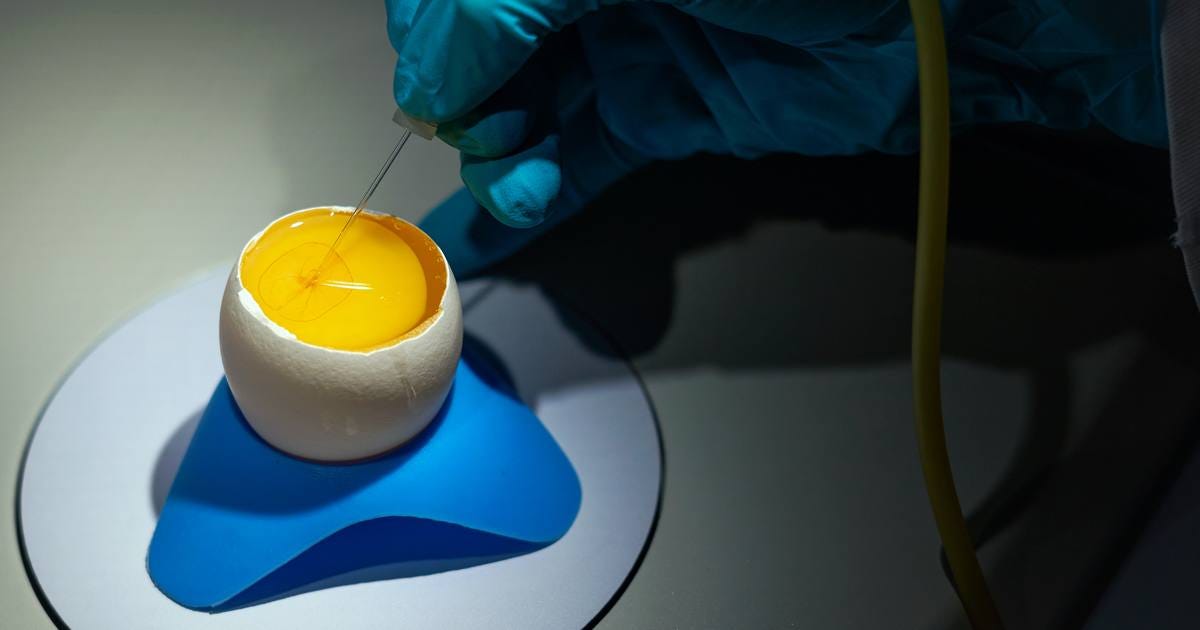

🥚 Neion Bio raised an oversubscribed $23M Series A to scale its egg-based biologics manufacturing platform

Neion Bio uses precision genetic engineering to turn chicken eggs into factories for complex, glycosylated proteins. Its Raptor™ platform restricts recombinant protein production to the egg itself, leaning on a vessel evolution and selective breeding have already optimised to produce and stabilise large quantities of protein in a sterile environment.

The company says the approach can produce biologics at meaningful scale within days, with advantages in scalability, resilience, capital efficiency, and cost over traditional bioreactors. It also claims the platform can express difficult-to-make proteins that have resisted conventional manufacturing, opening new product categories.

Proceeds fund pipeline expansion across biosimilars, innovative medicines, critical reagents, and animal health. The raise follows Neion’s March 2026 emergence from stealth and a first commercial co-development and supply deal with a major pharma company, a multi-product biosimilars collaboration for global markets.

Investors: Caffeinated Capital, Digitalis Ventures, Ensemble VC, Trust Ventures, Haystack, Basis Set Ventures

Source: BioSpace

Thoughts 🤔

The framing of the round is interesting. Both the CEO and Caffeinated Capital anchored the pitch on domestic supply chains and access to critical medicines, and that framing carries more weight now the BIOSECURE Act became law in December and biomanufacturing is treated as a national security domain. An oversubscribed round, in a market that has lost more than 200 biotechs to cash problems in four years, seems hard to explain on biosimilar economics alone.

A flock is domestic, distributed, and does not need a $500M facility, which maps onto the reshoring thesis neatly. I suspect the capital here is following the policy category as much as the cost curve, and if so, the framing that cleared this round also raises the bar later.

Worth noting the biology is not new. Alexion’s Kanuma was approved out of transgenic hen egg whites back in 2015, and egg-based production stayed a one-drug curiosity for the decade since while everyone kept building CHO capacity. That proven biology is reassuring for regulatory risk. This could become a platform if the differentiator is repeatability across proteins rather than the egg itself.

🌾 Leaf Agriculture raised $13M Series B to standardise farm data and power AI tools across agriculture

The US startup cleans and structures fragmented farm data so partners can build AI tools on top of it. Field devices store information like farm boundaries, product names, and agronomic practices in incompatible formats and calibrations. Leaf resolves this so the data is usable across pre-planning, planting, growing, harvesting, and selling.

Leaf positions itself as the infrastructure layer for agriculture, comparing its role to Stripe in payments or Plaid in banking: invisible to farmers but mission-critical for the companies building on farm data. The company says it processes data from over 20% of global acres annually, working with crop insurers, ag retailers, input companies, food processors, and commodity traders.

The funding lands in a tough farm economy where buyers are pushing to optimise operations and adopt AI. Leaf says the payoff shows up downstream. Crop insurance partners pay out claims in days rather than months, retail partners run field-specific seed and chemical models, and compliance partners open new revenue streams while saving farmers hundreds of hours of manual data entry.

Investors: Leaps by Bayer

Source: Leaf Agriculture

Thoughts 🤔

The round is a useful marker for where the binding constraint on agricultural AI sits. It is not the model.

A frontier system cannot just ingest farm data and produce useful agronomy, because that data arrives in incompatible OEM formats, proprietary calibrations, and inconsistent conventions. Reconciling it means knowing what a planting prescription, a harvest pass, or a soil result actually means. That is ag-specific knowledge encoded into the data layer, and the part horizontal AI does not bring with it.

A $13M Series B also seems modest for a company touching 20% of global acres, though that is not a knock and I am not encouraging companies to raise money they do not need! A business at that footprint pitching itself as critical AI infrastructure could plausibly command a larger growth round in a friendlier market. A small, strategically anchored cheque suggests the capital is buying ecosystem positioning as much as funding scale-up.

🤖 SWARM Engineering raised $10M to bring real-time AI decision-making to agri-food operations

The San Francisco-based startup’s platform takes in structured and unstructured data from ERP systems, spreadsheets, and real-time feeds, then runs scenario analyses across thousands of variables in minutes. Customers reach full operational use within 8-10 weeks, versus the 18-plus-month timelines of traditional ERP rollouts.

The platform is built on what the company calls an “operational ontology” of agri-food and manufacturing, embedding industry-specific decision logic, constraints, and variable relationships into its AI models. SWARM says this lets it work with fragmented, imperfect data rather than requiring deep ERP integration upfront.

Early deployments anchor the pitch. At Ardent Mills, North America’s largest flour miller, teams now simulate hundreds of logistics scenarios in one session vs a multi-day manual rebuild. Springs Window Fashions cut planning cycles 40% and freed working capital. Funds go toward new use cases, deeper ERP and supply chain integrations, and go-to-market expansion.

Investors: S2G Investments, AgRogue Growth Partners, Radicle Growth, Grit Road Partners, Middleland Capital, Open Prairie, Serra Ventures, and Trailhead Capital

Source: AgNavigator

Thoughts 🤔

SWARM is selling deployment speed as the headline differentiator: 8-10 weeks to production vs the 18-month ERP transformation that kills most enterprise planning deals. It works with fragmented, badly labelled data instead of demanding customers clean it first. As the model layer commoditises, that sequencing is the competitive axis.

The more durable asset is buried in how the CEO describes deployment. The most valuable part, he says, is mapping how decisions get made, including the informal constraints most operators cannot articulate. That is SWARM encoding tacit operational knowledge that “can take decades to accumulate” into a reusable structure. A single deployment improves one customer’s planning. A library of agri-food decision logic compounds across customers, because protein production, grain processing, and food manufacturing share constraint structures.

The asset that compounds is the decision data more than the AI. My guess is the advantage goes to whoever maps the most operating reality across the most sites, and the models increasingly just run on top of that layer.

🍬 Tate & Lyle expanded plant cell culture partnership with BioHarvest Sciences to develop multiple plant-based sweetener molecules

The British ingredient giant has broadened a collaboration it first struck with Canadian plant cell culture company BioHarvest Sciences in late 2024. The original deal aimed to create plant-based molecules that cut sugar in food and drink while addressing demand for affordable, sustainable, and nutritious alternatives.

The expanded scope now covers multiple sweetener molecules, giving manufacturers a flexible toolkit for different formulation needs. Tate & Lyle is betting that no single sweetener can deliver everything customers want (sugar-like taste, nature-anchored solutions, reduced calories), so it is developing complementary molecules usable independently or in tandem.

The work draws on BioHarvest’s Botanical Synthesis platform, a non-GMO technology that produces high-value plant compounds without growing the plants. It combines plant cell biology, elicitation, AI-driven development, and industrial bioreactors to make “precision botanics” it says offer enhanced potency, purity, consistency, and scalability.

Source: Green Queen

Thoughts 🤔

The timing of this partnership is interesting, as Tate & Lyle broadened a multi-molecule sweetener commitment just weeks before agreeing to a £2.7B all-cash takeover by Ingredion, with completion not expected until the second half of 2027.

Ingredion is buying Tate & Lyle largely for its sweetening and sugar-reduction book, the part carrying 16-18% operating margins against Ingredion’s ~9%. That makes the BioHarvest work less a standalone bet and more a feature of the asset being sold. Late-stage R&D expansions before an acquisition tend to do one of two things: build real pipeline depth, or signal to the acquirer that the franchise is worth paying up for. No molecule is named and no timeline disclosed, so it is hard to tell which from the outside.

Interesting to see whether Ingredion keeps funding the BioHarvest relationship after close, or quietly lets it lapse once the deal is locked.

🐛 Aphea.Bio partners with Bayer to co-develop bioinsecticides targeting sap-sucking pests

The partnership combines Aphea.Bio’s pipeline of bioactive microbial metabolites with Bayer’s global development, regulatory and commercialisation reach. First targets are fruit crops including pome, stone fruit, citrus and grapes, with scope to expand into vegetables and row crops like cotton and soybean.

The startup positions its metabolites as combining the environmental profile of biologicals with the stability and usability of conventional products, a barrier the industry has long struggled to clear. Sap-sucking insects are a growing problem as resistance and tighter regulation erode legacy chemistry.

Candidates advance through joint field validation and early regulatory work, with milestone gates tied to efficacy, safety and manufacturability. The deal adds to a wider push by agrochemical majors into biologicals.

Source: AgNavigator

🥛 Lacto Japan made a strategic investment in Leaft Foods to scale Rubisco protein for the Japanese market

The New Zealand startup extracts Rubisco, the most abundant protein on Earth, from alfalfa grown in Canterbury. It is a complete protein with a PDCAAS score similar to beef, egg whites, and dairy, and is rich in vitamins, minerals, and antioxidants. Functionally, it foams, gels, and emulsifies, setting like egg whites in baked goods.

Most methods for extracting Rubisco from green leaves destroy its delicate structure. Leaft Foods developed a gentle, food-safe process that preserves protein integrity. It positions the ingredient as an egg alternative for a supply chain hit by climate change and avian flu, and as a way to fortify dairy and non-dairy products.

The undisclosed investment deepens an existing collaboration to supply Japan’s largest food manufacturers, targeting revenues worth tens of millions of dollars within 5 years. Lacto Japan says the goal is to build a production and sales framework for Rubisco protein and strengthen the partnership.

Investors: Lacto Japan

Source: Green Queen

Thoughts 🤔

Leaft Foods has raised $15M so far and runs a demo plant making a tonne a week. Plantible already has US FDA clearance and a Texas facility producing hundreds of tonnes of Rubisco from lemna. Fudi is extracting from alfalfa on the same logic Leaft uses. On capital and capacity, Leaft is not the leader in this field.

What it has that the others do not yet is a locked route into Japan. Lacto Japan is a dairy ingredients trader, and its value to Leaft is decades of relationships with the country’s largest food manufacturers. Reading its own framing, the investment sits inside its whey protein book, where isolate prices are elevated on GLP-1 demand. A functionally comparable protein is a supply hedge it can sell through rails it already owns.

The differentiation in Rubisco is no longer who can extract but who can place it. If Leaft converts the Lacto Japan channel into signed manufacturer offtake before competitors establish their own Japanese routes, the early-mover lock on distribution likely matters more than its initial capacity disadvantage.

❄️ CryoVera taps an extremophile-inspired molecule to stop ice crystals from wrecking frozen food texture

The Paris startup is developing antifreeze ingredients that bind to ice crystals and block new water from building on top, preventing the recrystallisation that turns ice cream and frozen products gritty or crunchy. The molecule is inspired by an extremophile organism that survives extreme cold, though CryoVera is withholding specifics until its patent filings clear.

The real problem is not full thaw-refreeze cycles but the small, repeated temperature fluctuations frozen products face along the cold chain, down to shoppers opening freezer doors. CryoVera’s pitch is that ice recrystallisation inhibition assays show its molecules work at very low inclusion levels, keeping cost-in-use down for manufacturers.

The team extracts the molecules from abundant natural sources using microbe-secreted enzymes, a faster path to market while keeping precision fermentation on the long-term roadmap. CryoVera is sampling frozen bakery, ice cream, and other firms, with interest also from plant-based meat brands.

Source: AgFunderNews

Thoughts 🤔

Unilever’s ice structuring protein cleared EFSA, sold in the hundreds of millions of units, and still never reached the wider market. The GM yeast it was made with, and the “GMO ice cream” labelling fight that followed, were likely part of why.

CryoVera is going after the same problem and steering around that production choice, extracting its molecule from a natural source already in the US, EU and Canadian food supply, with precision fermentation pushed to the back of the roadmap. That sequencing sounds like a deliberate move to keep a clean-label story intact, and it only pays if that story survives regulatory classification.

The team is candid that the ingredient could land as a food or as an additive with an E-number in Europe. A food classification keeps the clean label but an E-number puts the kind of additive marker on the pack that reformulation teams are trying to strip off. The extraction is hard in its own right, by the team’s own account, but the labelling outcome is what decides whether solving it is worth much.

🌾 China’s 15th Five-Year Plan puts farmer modernisation at the centre of rural policy with a strong push on smart agriculture

China’s plan for 2026-2030 aims to lift comprehensive grain production capacity to ~725M tonnes by 2030, building on 2025 output of ~714.9M tonnes, the second straight year above 700M tonnes. The framing extends beyond yield to transforming farmers from traditional producers into participants in technology-driven agriculture.

The plan places strong emphasis on smart agriculture, advanced machinery, improved seed systems, and digital tools, including AI, to raise productivity and ease labour constraints. It also pushes farmers beyond primary production toward rural industry, employment, and entrepreneurship to diversify income.

The Ministry of Agriculture and Rural Affairs called agricultural and rural modernisation its “most arduous and challenging task” and described it as “lagging behind,” warning that “without agricultural and rural modernisation, there can be no modernisation of the entire country.”

Source: AgNavigator

🏭 Biomanufacturing as industrial infrastructure: Why operating biology, not just designing it, is now the strategic prize

The global bioeconomy is worth $4-5T, with potential to reach $30T by 2050, and 50+ countries now have a national bioeconomy strategy. The resilience case is structural: chemicals and materials supply chains are concentrated in a few countries with oil, large agricultural bases, or specific processing capacity, which makes them fragile. Biomanufacturing offers a different geometry, with production sited regionally on local feedstocks.

Most AI excitement in biology points at discovery: designing strains, predicting structures, accelerating R&D. That work addresses only half the problem. Shannon Hall argues the bigger unlock is operational. ML, digital twins, and predictive process control stabilise and transfer living processes in real time, encoding bioprocess knowledge into models that travel between sites.

For policy-makers, Shannon says treating biology as strategic infrastructure means three shifts. Fund the manufacturing layer (pilot facilities, shared infrastructure, transferable data systems), not just discovery. Structure public-private investment for long horizons. Invest in the workforce and tools that let a distributed network function as one.

Source: World Economic Forum

Thoughts 🤔

Most attention on AI in biology has gone to discovery: designing strains, predicting protein structures, accelerating R&D. This piece is useful because it names the half that gets ignored.

Worth flagging that Shannon’s company, Pow.Bio, sells this kind of operational tech, so the framing is partly promotional, but the underlying point stands. The harder problem is operational: how you stabilise, transfer, and run living processes economically at scale. That is where most fermentation companies die, and the application of AI I am most interested in right now.

The policy asks land in the same underfunded place. Most bioeconomy strategies still skew toward research, so funding the manufacturing layer (pilot facilities and the shared data infrastructure that makes processes portable) targets the messy middle between lab and commercial scale that VC has retreated from.

The strongest of the three asks is funding shared, transferable-data infrastructure, because that is the part no single company can justify building alone and the part that determines whether a distributed network functions as a network. If private investors will not fund these facilities, governments have to step up.

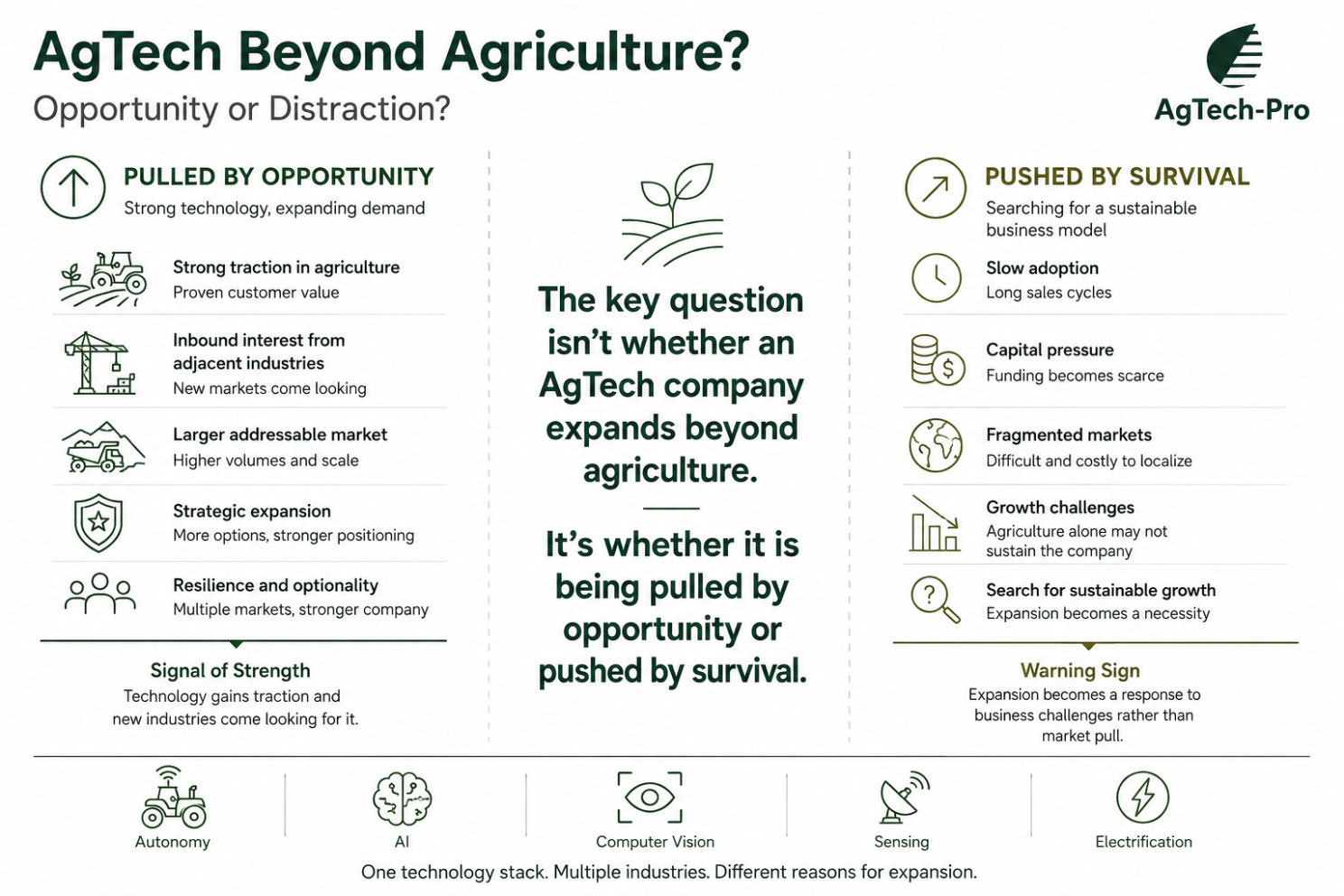

💭 Is AgTech leaving the farm?

Patrick Honcoop observes that AgTech companies, especially in automation, robotics, and sensing, are increasingly eyeing adjacent industries as their next market. Two recent deals make it visible. In April 2026, Caterpillar acquired the assets of Monarch Tractor, an autonomous electric tractor startup. In May 2026, Elbit Systems’ subsidiary FUSE acquired Bluewhite, an Israeli autonomy platform built for California permanent crops with 100,000+ hours of field operation. Neither buyer was an agriculture company.

Patrick argues the pull is economics. A robotics company serving California almonds has a TAM in the hundreds of millions. The same autonomy stack pointed at construction, mining, and defence scales into the billions, and volume drives down per-unit cost on hardware that stays expensive because ag volumes are low. Defence has also turned investable again as NATO spending and geopolitical tension reframe dual-use tech.

His framing splits the move two ways. Some founders are pulled outward by inbound interest after building something valuable in ag. Others are pushed out because the unit economics fail in a fragmented, seasonal, low-margin market. His warning: agriculture can become secondary by resource allocation rather than deliberate choice, leaving companies that serve everyone adequately and no one exceptionally well.

Source: Patrick Honcoop/LinkedIn

CAPITAL & CONVICTION

The sharpest thinking in agrifood tech often happens off the record. My interview series brings it on the record:

Agtech’s Real Bottleneck Is the Translational Layer, Not the Technology - Beanstalk AgTech’s Justin Ahmed

Why 2026 Is the Great Shakeout Year for Food and Ag Tech - EcoTech Capital’s Adam Bergman

What It Takes to Build a Fundable Food Company After “Peak Stupid” - Siddhi Capital’s Steven Finn

Engineering the Exit: How to Get Acquired in Deep Tech - SOSV’s Cyril Ebersweiler

How Agrifood Tech Investing Is Shifting and Where Value Will Be Created - PeakBridge’s Yoni Glickman

Browse the full archive. More conversations dropping soon. Stay tuned!

Thanks for reading!

Let me know your thoughts in the comments or by replying to this email. If you want to connect with me on LinkedIn, you can find me here.

If you found value in this newsletter, consider sharing it with a friend who might benefit! Or, if someone forwarded this to you, consider subscribing.

Disclaimer: The views and opinions expressed in this newsletter are my own and do not necessarily reflect those of my employer, affiliates, or any organisations I am associated with.