Precision-Fermented Egg Protein Orders Jump 550%, and EU Rewrites Gene-Editing Rules

Also: Döhler acquires cocoa-free chocolate startup, Rainbow Crops raises €9.7M for AI-guided multiplex editing, and Singapore's new synbio lab to speed bio research to market

Hey, it’s Eshan. Welcome to Issue #150 of Better Bioeconomy, insights on companies, capital, and ideas reshaping food, agriculture, and biomanufacturing for human and planetary health. Thanks for being here!

This week, Vivici pulled €12.5M from the EIC to scale its cow-free whey, while Helaina pushed its precision-fermented breast-milk protein into kids’ multivitamins. Rainbow Crops raised €9.7M seed round to scale AI-guided multiplex gene editing, and The Every Company quadrupled its egg-protein capacity on a pharma partner’s idle fermenters.

On the institutional side, A*STAR and NUS launched a synbio joint lab in Singapore, Döhler acquired Nukoko’s fava-bean chocolate, and Anterra closed $100M to rewire the food system rather than reinvent it. I also dig into what agtech can learn from biotech about VC returns.

Below are the 10 most interesting ag and food tech stories I came across last week, paired with my thoughts on what they mean for where the industry is heading.

🥚 The Every Company quadruples precision-fermented egg protein capacity with Huvepharma after 550% hike in orders

The animal-free egg protein maker has expanded its partnership with pharma manufacturer Huvepharma to scale OvoPro production fourfold, tapping subsidiary Biovet’s 9M-litre fermentation facility in Bulgaria. The precision-fermented egg white protein already features in products at Walmart, Target, and Amazon.

The startup says it secured annual orders worth 55% of its total 2025 order volume in just the first four months of this year, driven by B2B retail, e-commerce, and foodservice adoption. It had already doubled capacity at the start of 2026 with plans to double again next year, but the surge accelerated that schedule.

OvoPro is positioned as a hedge against a volatile egg supply chain hit by bird flu and price spikes. The company says it is shelf-stable for up to 24 months, needs no cold chain, and is priced competitively with or cheaper than battery-caged commodity eggs on a cost-in-use basis.

Source: Green Queen

Thoughts 🤔

One of the biggest bottlenecks for scaling biotech-derived food ingredients is the lack of fermenters at a scale that justifies the cost. The space badly needs more food-grade capacity to support scale-ups.

A greenfield food-grade plant runs hundreds of millions of dollars with multi-year lead times, roughly the cost structure that sank the first full-stack precision fermentation (PF) wave. Pharma fermentation already carries EU and US FDA GMP approvals, sits at industrial scale, and is sometimes underused. Renting into that base, then converting a site as volumes justify it, sidesteps both the CAPEX and the time. It works only because food protein can clear pharma-grade process bars, not the reverse.

Expect more food PF to scale on someone else’s depreciated steel rather than its own balance sheet. The catch is that this only works where pharma capacity is both idle and willing to convert to food use. That pool is smaller than the 9M-litre headline suggests, and once a site goes fully dedicated to one customer, both sides inherit the single-tenant risk that makes fermentation capacity so hard to underwrite in the first place.

🧬 Rainbow Crops raised €9.7M seed round to scale AI-guided multiplex gene editing for complex crop traits

The Belgium-based startup, spun out of research institute VIB in 2025, uses AI to predict which gene combinations drive complex traits like drought tolerance and higher yield, then applies multiplex editing and breeding to create populations of edited plants for high-throughput screening. The traits it targets are polygenic, controlled by networks of interacting genes rather than one.

Rainbow Crops claims an edge in multiplexing, editing 50-100 genes at a time rather than a handful, and is moving beyond simple knockouts toward tuning regulatory elements to dial gene expression up or down. It says its approach generates many edit combinations from a single transformation event, easing the burden in crops that are hard to transform or slow to regenerate.

The model is to license platform output to seed and breeding companies with strong germplasm but limited editing capability. Rainbow Crops earns royalties on commercialised varieties plus upfront R&D fees and milestone payments, and expects to announce a corn collaboration soon.

Investors: LIFTT EuroInvest, AIF (Agri Investment Fund), PINC, VIB, Maia Ventures, Corteva Catalyst

Source: AgFunderNews

Thoughts 🤔

What I find interesting about this round is how much VIB de-risked the company before venture money came in. By the time investors wrote the cheque, the science was already well advanced and validated in greenhouse and early field trials. That is uncommon at seed stage and worth paying attention to.

Rainbow did not spin out in 2025 as an idea and then go raise. The yield-gene science was matured for years inside VIB, an entrepreneur-in-residence was brought in specifically to commercialise it, the company gets access to VIB’s transformation and automated phenotyping facilities that screen up to 16,000 plants at once, and a Gates Foundation grant landed three months before this close. Those are resources a startup at this age rarely has, and the result looks unusually mature for its stage.

Investors are pulling back from early-stage capital. A studio that absorbs the science risk upstream is one way to make a young company look fundable in a market that no longer wants to underwrite raw technical risk.

🥛 Vivici secured €12.5M from the European Innovation Council to scale its cow-free whey proteins

Vivici makes animal-free dairy proteins via precision fermentation, sold under its Vivitein brand. The Dutch startup secured €12.5M in blended grant-and-equity finance through the EIC’s 2026 accelerator, one of 38 businesses picked from 87 proposals. The capital expands supply and market access for its whey ingredients.

Its flagship Vivitein BLG is a bioidentical beta-lactoglobulin prized for gelling, foaming and binding. It carries all essential amino acids, runs clear and neutral in flavour, and works at up to 50% by weight in meal replacements, functional drinks, nutrition bars and dairy analogues.

Earlier this year, Vivici added Vivitein LF, an animal-free lactoferrin at 95% purity targeting gut health, recovery and women’s wellbeing verticals. The company has tested its process in a 75,000-litre fermenter and works with co-manufacturers in Europe and the US for commercial-scale output.

Source: Green Queen

Thoughts 🤔

Great to see Europe putting public money behind fermentation scale-ups. Vivici added a blended EIC grant-and-equity package a year after its Series A, and in the same week Solar Foods drew €77.8M from Business Finland for its second factory.

The instruments are not identical, Solar Foods is roughly half repayable IPCEI-linked debt while Vivici’s is grant plus patient EIC Fund equity, but the direction is shared: European public capital is stepping into the part of the curve where private venture has pulled back.

That part is scale-up, and it is capital heavy. Commercial-scale fermenter capacity costs a lot, and the climb from a validated process to positive unit margins can run years. Grants and concessional equity are built for exactly this, longer timelines and softer return expectations.

🏛️ EU adopts product-based gene-editing rules, clearing a faster path to market for NGT crops

The European Parliament has adopted new rules for plants made with new genomic techniques (NGTs), finalising a process that began with a provisional Parliament-Council deal in December 2025. The reform shifts the EU from process-based to product-based oversight, assessing plants on their genetic traits rather than the technique used to make them.

A two-tier system splits the field. NGT-1 covers edits comparable to conventional breeding, which, once verified, are treated like conventional crops, listed in a public EU database, and labelled as NGT-1. Herbicide-tolerant and insecticidal traits are excluded. NGT-2 covers more complex modifications and stays under existing GMO rules, including risk assessment, authorisation, and full traceability.

The framework aligns the EU with the US, Brazil, and parts of Asia, where gene-edited crops already reach markets, and applies equally to domestic and imported products. It validates the regulatory philosophy long pushed by Bayer, Syngenta, and Corteva, preserves the option to patent NGT innovations with safeguards on market concentration.

Source: AgNavigator

Thoughts 🤔

One way I’m reading the EU’s NGT decision is through the question Europe asks before letting a plant in.

The old GMO regime asked how a plant was made, so using a new genomic technique triggered strict authorisation no matter the result. The new rules ask what is in the plant instead. NGT-1 edits, the kind achievable through conventional breeding, get verified on their genetic characteristics and then treated like conventional crops.

The EU was one of the last major agricultural market still regulating by process while the US, Brazil, and parts of Asia had moved to product-based pathways. Traits cleared abroad still hit a separate, slower hurdle in Europe.

The catch is that judging a trait on its characteristics does not automatically make it quick to place. The whole fast-track promise rests on how NGT-1 verification actually runs once the secondary legislation defines it.

If verification is quick and predictable, the product-based question becomes a fast lane. If it turns into a slow case-by-case assessment, the shift is real on paper but the timeline advantage is smaller than the headline suggests.

💊 Helaina’s precision-fermented human lactoferrin moves into kids’ multivitamins via Vital Nutrients

US supplements brand Vital Nutrients has launched Mighty Multivitamin Without Iron, a gummy for children aged 2 and up built around effera, Helaina’s recombinant human lactoferrin. The ingredient is paired with six fruit and vegetable concentrates, minerals, and vitamins A, B, C, D and K1.

Lactoferrin is a whey protein found in human breast milk and bovine colostrum, with far higher concentrations in the former. Helaina uses precision fermentation to make a bioidentical version of the human protein, sidestepping the supply limits of dairy-derived lactoferrin.

The launch pushes precision-fermented breast milk proteins into children’s nutrition, a new application alongside Helaina’s existing targets across functional foods, longevity, women’s health, and infant formula. The product is free of the top 9 allergens, gelatin and pectin, and Vital Nutrients says adults can take the meltable tablets too.

Source: Green Queen

Thoughts 🤔

Clearing the steepest trust bar in supplements, children’s nutrition, with a recombinant breast-milk protein is a strong vote of confidence. It also sits one step below the highest-stakes application of all, infant formula, which is exactly where Helaina is heading after signing a Nestlé formula deal with effera this month.

A kids’ multivitamin seems like a controlled, low-dose way to normalise a human-identical milk protein in a child-facing product before the formula conversation gets real. If the kids’ products gain shelf trust without safety or labelling friction, it strengthens the case for the formula play.

🍫 Döhler acquired Nukoko to scale cocoa-free chocolate made from fava beans

The German ingredients giant has bought the UK startup behind a cocoa-free chocolate built on fava beans, two years after first investing in the company. The deal folds Nukoko’s approach into Döhler’s wider plant-based ingredients portfolio, pairing the startup’s biotech platform with Döhler’s flavour and formulation expertise.

Nukoko puts fava beans through a biotransformation and controlled fermentation process before drying, roasting, and grinding them into a cocoa-style powder. It claims the product generates 90% fewer emissions and carries 40% lower sugar with no hit to taste, alongside higher protein and fibre.

Cocoa prices have swung violently, and Döhler is positioning fava-bean chocolate as a hedge against that volatility for confectionery makers. The acquisition lets Döhler offer customers a ready alternative across formats from confectionery to baked goods and ice cream, moving the technology from early-stage concept to market-ready ingredient at scale.

Source: Green Queen

Thoughts 🤔

Döhler invested in Nukoko two years ago at pilot stage, watched the process de-risk through its transition toward 10,000-litre batches, then bought the whole thing once the technical risk was largely retired. That is corporate venture used as a staged option on process IP.

It works because Döhler already had everything except the process. It is deeply vertically integrated across pulses, seeds, and nuts, with the distribution and formulation muscle to take an ingredient to market. What integration in raw materials does not give you is a fermentation-and-roasting route that turns fava vicilin into chocolate notes.

Döhler clearly bought more than that, a brand, a patent-pending portfolio, a team, and a B2B pipeline, but the piece I find hardest to build in-house, and the one that looks most like the prize, is that biotransformation. On that read, the acquisition takes a route off the table that rivals would now have to build themselves.

This is more a template than a chocolate story. Expect more ingredient majors to run CVC stakes explicitly as acquisition options on de-risked process IP, leaving founders a clean exit and the major a capability it can keep in-house.

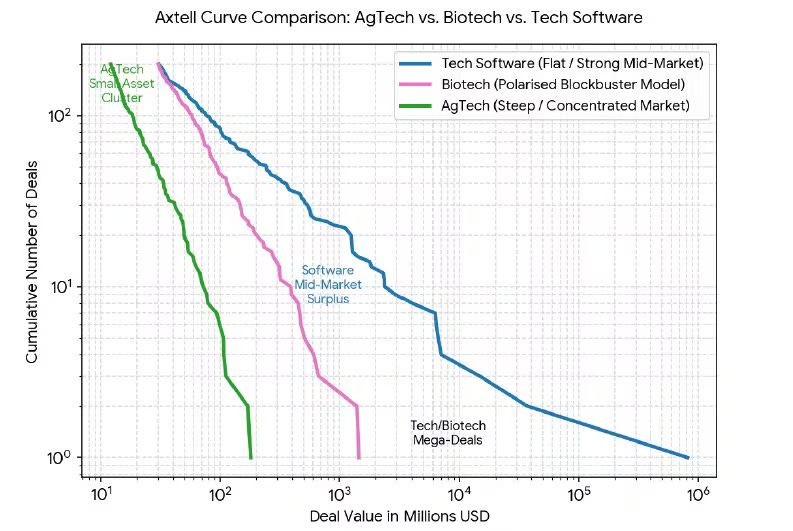

🤔 What can agtech learn from biotech about VC returns?

Michael Lee, managing director at Syngenta Group Ventures, argues agtech should borrow lessons from biotech, a structurally similar but far larger VC arena. Healthcare is ~17% of US GDP vs agriculture’s ~0.9%, a 20:1 gap that shows up across exit metrics. Biotech has 1,000+ buyers, while agtech relies on a handful of agchem and tractor makers, collectively closing just 1-2 deals over $20M annually.

Plotting deal frequency against deal value, Lee finds agtech M&A clusters tightly in the $30M-$100M band before dropping off sharply, leaving almost no mid-market and no path to large standalone exits. The top 20 non-SPAC agtech exits over 20 years averaged $400M. Back-solving from that with 3x step-ups implies tight round valuations: ~$8M pre at seed, ~$25M at Series A, ~$100M at Series B. Inflated intermediate valuations, he says, are toxic to both returns and company survival.

Lee flags vertical farming and row-crop genetics as poor fits for VC, citing airline-like economics of high CAPEX, long timelines, and weather and commodity volatility. His prescription: laser focus on entry valuations, avoid companies that have raised over $50M, look for pre-acquisition collaboration signals, and actively widen the buyer universe into food, climate, fintech, and AI-enabled players.

Source: Ag Tech Navigator

Thoughts 🤔

Biotech and agtech are, in my view, very different underneath the similarities Michael starts with. Long timelines, regulatory gauntlets, efficacy trials: the surface case for treating them alike is real. But the one variable that sets valuations runs the opposite way in each. Health is inelastic demand. Food is elastic and commodity-priced.

Michael gives the mechanism in a single line that deserves more weight. A 10% yield gain is priced at the value of the extra yield minus any change in input cost, a hard arithmetic ceiling. A 10% improvement in an oncology outcome is priced at whatever someone will pay to live.

One number is bounded by a commodity price the grower does not control, the other by willingness to pay with almost no ceiling. That is why biotech sustains a premium agtech has not been able to command at scale. Everything downstream follows from that gap.

You might think the ‘food is medicine’ shift rescues this from above, with consumers paying more for better food. But that is a different buyer at a different layer. The grower buying a seed trait is not the shopper buying the product, and where a wellness premium does exist, it has mostly stayed downstream with the brand rather than flowing back to the trait or the input that created it.

🤝 A*STAR and NUS launch a synthetic biology joint lab to move Singapore’s bio-based research closer to market

The new joint lab pairs A*STAR’s Singapore Institute of Food and Biotechnology Innovation, which brings bioprocess development and scale-up know-how, with the National University of Singapore’s synthetic biology group, which contributes fundamental science and talent development. Its initial focus is nutrition and consumer care, with broader applications across advanced materials and health.

The lab targets three areas to speed up translation: AI-guided enzyme and pathway engineering to shorten development timelines, industrially deployable microbial platforms to make complex molecules at scale, and access to novel bio-based compounds for ingredients and functional applications. It will work with companies to co-develop, test, and validate sustainable alternatives to conventional chemical manufacturing.

Beyond R&D, the lab doubles as a training ground for synthetic biology, metabolic engineering, and industrial biomanufacturing talent through joint supervision, internships, and fellowships. Demand for these skills is rising as more companies build in-house biotech capabilities.

Source: NUS News

💰 Anterra Capital raised a $100M first close on Fund III to “rewire” the food and agriculture system

Anterra is an agrifood VC that backs companies fixing the existing food system rather than new categories. The maths drives the thesis: the meat industry is worth close to $2T, the alt-meat market $10-20B. Founding partner Maarten Goossens argues there is more value in rewiring the bigger system than in reinventing the smaller one.

The fund targets $200M total and has already made 2 investments. One is veterinary biologics company Animerra, which Anterra founded and funded in-house. The firm builds startups from within its own walls, a model that produced 3 companies in Fund I and 7 in Fund II, with a target of 7-10 for Fund III.

Anterra is also leaning into vertical AI, backing Anchr, an agentic platform tackling inefficiencies across the seafood chain from vessel to restaurant. Goossens says the firm benchmarks against general VC rather than niche agrifood peers, and claims Funds I and II are delivering top-tier returns.

Source: AgFunderNews

🐄 Deco Labs upcycles canola oil waste into a plant-based albumin replacement that cuts cultivated meat’s most expensive media cost

The Tufts spinout’s cAlbumin is a protein isolate extracted from rapeseed meal, a canola oil byproduct normally destined for livestock feed. It drops in for both bovine serum albumin and recombinant versions, the single most expensive ingredient in serum-free culture media.

Conventional albumin and transferrin together add nearly $100/kg to cultivated meat production. Deco Labs says cAlbumin contributes ~$0.02 per litre of media at scale, works at lower concentrations, and has outperformed both recombinant and bovine albumin across more than a dozen cell types.

GFI estimates the industry could need up to 10,000 tonnes of albumin by 2030, volumes that don’t yet exist. Deco is validating every batch for 10+ cell doublings before shipping and is already sampling cultivated meat, seafood, leather, and collagen firms, plus cell therapy and vaccine manufacturers. A pipeline of amino acid (cAminos) and FGF-2 (pFactor1) replacements is in development.

Source: Green Queen

Thoughts 🤔

Some companies are trying to engineer albumin out of the process entirely, adapting cells to grow without it. Deco is making the opposite bet. Its thesis rests on the claim that albumin-free cells underperform at scale, so the smarter move is supplying a cheap drop-in replacement rather than removing the protein company by company.

That is what makes the supplier position attractive: a rapeseed isolate at ~$0.02/L sells into most cell lines, where removal has to be re-solved by each producer.

cAlbumin is being sampled by cell therapy, regenerative medicine, and vaccine manufacturers, not just meat and seafood startups. With cultivated meat funding down and companies shutting down, tying the company to that market alone would be fragile. Biopharma media is growing the other way. The biopharma-adjacent demand likely carries Deco near-term, with cultivated meat as the upside.

CAPITAL & CONVICTION

The sharpest thinking in agrifood tech often happens off the record. My interview series brings it on the record:

Agtech’s Real Bottleneck Is the Translational Layer, Not the Technology - Beanstalk AgTech’s Justin Ahmed

Why 2026 Is the Great Shakeout Year for Food and Ag Tech - EcoTech Capital’s Adam Bergman

What It Takes to Build a Fundable Food Company After “Peak Stupid” - Siddhi Capital’s Steven Finn

Engineering the Exit: How to Get Acquired in Deep Tech - SOSV’s Cyril Ebersweiler

How Agrifood Tech Investing Is Shifting and Where Value Will Be Created - PeakBridge’s Yoni Glickman

Browse the full archive. More conversations dropping soon. Stay tuned!

Thanks for reading!

Let me know your thoughts in the comments or by replying to this email. If you want to connect with me on LinkedIn, you can find me here.

If you found value in this newsletter, consider sharing it with a friend who might benefit! Or, if someone forwarded this to you, consider subscribing.

Disclaimer: The views and opinions expressed in this newsletter are my own and do not necessarily reflect those of my employer, affiliates, or any organisations I am associated with.